ASphotowed/iStock via Getty Images

Article Thesis

Canadian banks have been strong investments in the past, due to above-average recession performance and since they tend to offer robust dividend payments to their owners. The Toronto-Dominion Bank (NYSE:TD) and Royal Bank of Canada (NYSE:RY) are two of the largest Canadian banks. In this article, we’ll pit them against each other to see which bank might be more suitable for different types of investors.

Unless noted otherwise, all numbers in this article are in US Dollars.

Are TD Bank And Royal Bank Of Canada Worth Investing In?

I do believe that the answer to that question is yes. Both banks have generated solid and reliable returns for their investors in the past:

Both banks have offered relatively comparable returns of around 180%-190% over the last decade, including dividend payments. This pencils out to annual returns of roughly 11% for both companies, which is very solid. The broad market offered higher returns in that time frame but was much more volatile. In fact, TD and RY both have a beta of just 0.5, which makes them quite attractive from a risk-reward perspective, I believe. Returns are not ultra-high but still compelling and very reliable, which is, at least partially, explained by their generous dividend policies.

How Are TD Bank And Royal Bank Of Canada Different?

Both banks operate in Canada primarily, and both companies have relatively comparable market capitalizations of around $130-$140 billion. Both companies also belong to the world’s top 10 banks in terms of market capitalization, which can be explained by the fact that equity investors reward them for their consistency and generous shareholder payout policies.

Nevertheless, there are some differences between these two Canadian banks. Royal Bank of Canada operates in Canada, the US, and in what it calls international markets:

RBC presentation

Its non-Canada businesses generate more than 40% of the bank’s revenue. Canada is still the most important market by far, but the bank nevertheless has considerable exposure to both the US and other international markets, including countries in the Caribbean, Europe, the Middle East, and so on.

Toronto-Dominion, on the other hand, is putting more focus on its home markets. It only operates in Canada and the US. The US Retail business is responsible for a little less than 30% of its profits, with the remainder being generated by the Canadian Retail and Wholesale business, as well as by an investment stake in publicly-traded Charles Schwab (SCHW).

Toronto-Dominion is larger in terms of total assets and deposits, but slightly trails Royal Bank Of Canada when it comes to profits and market capitalization.

TD And RY Stock Key Metrics

During the most recent quarter, Royal Bank of Canada managed to generate net profits of C$4.1 billion, which is equal to around $3.2 billion, or close to $13 billion annualized. The company’s strong profitability in both the recent quarter and previous ones, combined with a conservative approach by management, has resulted in a very strong capital position. The bank’s common equity tier 1 ratio (CET1) stands at 13.5%, which is well above average for major banks. If the bank wanted to, it could draw down that ratio over the coming years in order to boost shareholder returns.

But even without using available balance sheet flexibility, the bank offers strong shareholder returns to its owners. Between 2011 and 2021, Royal Bank of Canada has raised its dividend by 110%, or around 8% a year. In 2022, the bank will likely pay out C$4.80, or $3.72. This pencils out to a dividend yield of 3.7% at current prices, which is pretty strong compared to the dividend yields offered by most US-based major banks. At the same time, the combination of a yield of close to 4% and a (historic) dividend growth rate of 8% looks compelling for dividend growth investors. There’s no guarantee that dividends will grow at the same rate going forward, but thanks to RY’s strong track record and due to the fact that its payout ratio is pretty low, at just above 40%, I do believe that there is a high likelihood that investors will get meaningful and reliable dividend increases in the future, too.

Toronto-Dominion has generated net earnings of C$14.6 billion during 2021, which pencils out to $11.3 billion. This was way more than during the previous year, which can be explained by the lower provisioning for credit losses that the bank undertook in 2021, compared to the previous year where the pandemic impact was larger. That being said, its fourth-quarter profits were below the level from the previous year’s quarter, which was caused by lower revenue generation that could not be offset by lower expenses. Still, even in that quarter, TD remained very profitable, generating C$3.8 billion of net profits, which is equal to $2.9 billion. Toronto-Dominion’s common equity tier 1 ratio was 15.2% at the end of the most recent quarter, which is even stronger than that of Royal Bank of Canada.

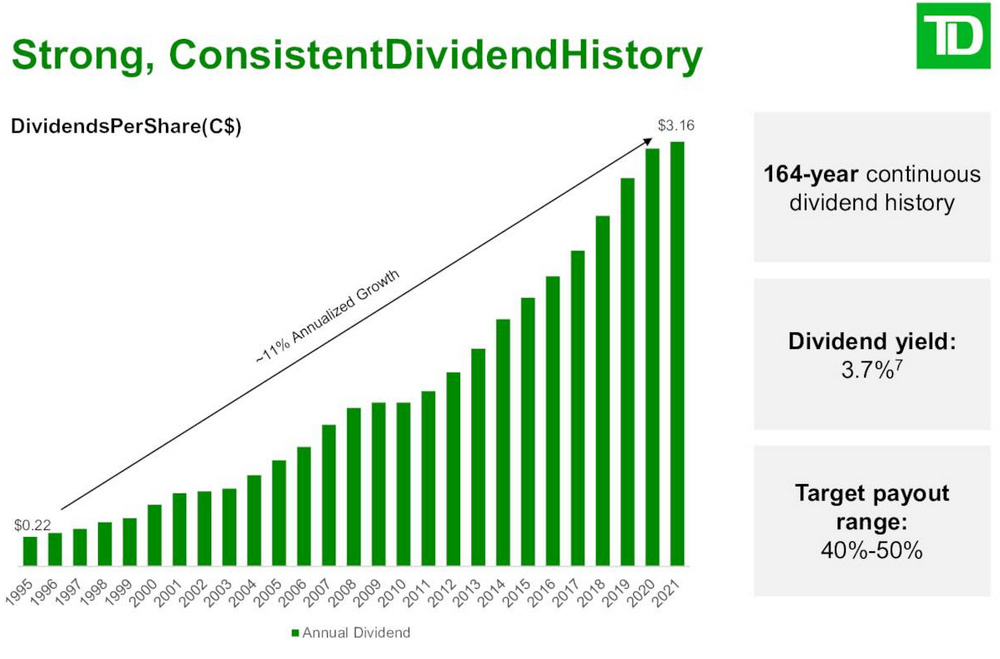

Toronto-Dominion’s dividend history is excellent:

TD presentation

Toronto-Dominion has made dividend payments for a very impressive 164 years, and the company has raised its dividend very consistently in the recent past. Between 1995 and 2021, the dividend has grown by 1,300%, or 11% annualized. That growth has slowed down to some degree in recent years, but even the 5-year dividend growth rate is at a pretty attractive level of 8.2%. At current prices, Toronto-Dominion offers a dividend yield of 3.8%.

We can thus say that Toronto-Dominion offers a slightly higher dividend yield and has a better dividend growth track record, while also operating with a higher CET1 ratio compared to Royal Bank of Canada. That being said, RY looks pretty good on those metrics as well, and it has a slightly lower dividend payout ratio (42% versus 44% for TD).

What Is The Outlook For TD And RY Stock?

Both companies are good investments from a fundamental basis, but of course, valuations have to be considered as well when making investment decisions.

Both banks are currently trading at almost the same valuation, as TD is valued at 11.4x this year’s earnings per share estimate, while the multiple is 11.5 for RY. Both companies trade at a small discount compared to how they were valued, on average, in the past. A return to the historical valuation norm would allow for upside potential of around 7%-8% for both companies.

When we add the fact that both companies should grow their earnings per share over time, through business growth and buybacks, and when we account for the attractive dividend yields of both banks, one can argue that both companies look like attractive investments today.

Analysts are currently predicting that Toronto-Dominion will grow its earnings per share at close to 8% a year going forward, while Royal Bank of Canada is forecasted to generate earnings per share growth of 4% a year. I personally do believe that the discrepancy will likely not be this wide in the coming years, mainly due to the fact that both companies grew their earnings per share almost perfectly in line with each other in the past. A sudden large divergence of this magnitude thus does not seem very likely to me, although TD still gets the point for the somewhat better growth outlook going forward. That being said, even a 4% earnings per share growth rate is far from bad when combined with a yield of close to 4% and a discount to the historic valuation norm.

Is TD Bank Or Royal Bank Of Canada Stock The Better Buy?

Both companies are fundamentally strong, have performed well during the pandemic and past recessions when compared to many other financial institutions, and both offer a sizeable dividend yield while trading at an inexpensive valuation.

However, Toronto-Dominion still wins this one, I believe. Its dividend yield is a little higher, its dividend growth a little bit faster, its expected earnings per share growth is better than that of Royal Bank of Canada. On top of that, Toronto-Dominion also has the higher CET1 ratio which makes it even more stable and reliable compared to Royal Bank of Canada.

Royal Bank of Canada does not perform badly when it comes to these metrics at all, but Toronto-Dominion is looking a little bit better, which is why I see it as the more favorable pick. That being said, one can of course own both, as both banks seem like suitable picks for a low-risk, reliable dividend growth portfolio.

Source: seekingalpha.com

{kind=link}

{kind=link}