The UK food sector is on the path to serious decline. That’s the stark conclusion of the House of Commons Environment, Food and Rural Affairs Committee’s recent report on labour shortages in the industry.

Pointing to supply chain disruption, unharvested crops and the culling of healthy pigs as examples of issues that are currently blighting the sector, the committee warned that the UK market “faces permanent shrinkage if a failure to address its acute labour shortages leads to wage rises, price increases, reduced competitiveness and, ultimately, food production being exported abroad and increased imports”.

Striking stuff. And it is inarguable that the food sector is struggling mightily with labour problems. This is partly Brexit-induced, given the outflow of European workers and a new immigration framework, and partly pandemic-driven, due to a quicker-than-expected recovery, which has left operators exposed against a tightening labour market.

The sector is now also dealing with the not so insignificant matter of major supply disruption for vital commodities such as wheat and oil due to Russia’s invasion of Ukraine. The situation is driving up prices, as well as impacting food security, with the conflict’s impact on supply fast becoming “apocalyptic” to quote Bank of England governor Andrew Bailey.

But these – very serious and pressing – issues shouldn’t obscure the great transformation that is taking place in the food sector. Driven by new technologies and consumer trends, from cultured meat to ‘flexitarianism’ – eating meat only rarely – and from indoor farming to the increasing awareness and application of environmental, social and governance (ESG) principles, there are major opportunities on offer for both companies and investors. With new post-Brexit legislation emerging in the UK on genetic technology, and a national food strategy, there is also the hope that regulatory divergence could offer some unique opportunities in the domestic market.

A complex food landscape

As it stands, the Organisation for Economic Co-operation and Development and the Food and Agriculture Organisation of the United Nations forecast that the global consumption of meat proteins will increase for the foreseeable future. Their joint ‘Agricultural outlook 2021-2030’ report projects a 14 per cent increase in consumption by 2030, driven by population and income growth.

On the face of it, this looks good for London-listed companies such as meat producer Cranswick (CWK) and sausage casings maker Devro (DVO). But when it comes to high-income countries such as the UK, the joint report says that concerns around health and sustainability issues are limiting meat consumption growth and this, combined with slower population growth, “will lead to a levelling off in per capita meat consumption”.

In fact, in the UK, there has been a decades-long trend of lower consumption of farmed animal proteins. Analysis in The Lancet Planetary Health journal found that average meat consumption per capita per day fell from 104g to 86g between 2008 and 2019. This trend is expected by analysts to continue, despite global demand rising.

The rise in vegetarianism and veganism is particularly noticeable amongst the younger generations, with around a third of UK generation Z and millennials agreeing with the statement that ‘a meatless diet is the healthier option’ in a YouGov (YOU) survey earlier this year – and those who hold this view are three times more likely than the average person to be vegetarian. Analysis in the same survey noted the most popular diet choice for those in agreement with the statement was flexitarian.

The Office for National Statistics (ONS) added meat-free sausages to its inflation shopping basket in March, “reflecting the growth in vegetarianism and veganism” in the UK, displaying the direction of travel well. Alongside this comes increased interest in dairy alternatives from ESG-conscious consumers in the market – the milk dairy industry contributes more CO2 emissions than aviation.

A growing health-consciousness can be seen in the results of a company such as Treatt (TET). Its healthy living categories, which cover its tea, health and wellness, and fruit and vegetables segments, have driven a significant portion of growth over recent years, with 29 per cent of revenue taken by these categories in the latest financial year. While management doesn’t give forward guidance for categories, long-term historic double-digit growth in this area of the business makes the outlook an optimistic one. Analysts (based on consensus forecasts) expect Treatt to hit £143mn in sales and earnings per share of 28p for its 2022 financial year, which would represent growth of around 15 per cent on both metrics.

Demography is a central part of the background to the food revolution. While there are major differences in population growth rates across the developed and developing world, the global population is expected to rise to around 10bn people by 2050. There will be heightened demand for crops, meaning that the food system simply needs to produce more. Bank of America (BoA) analysts said in a recent report that “we need to produce more food in the next 40 years than we have harvested in the past 8,000 years” which is quite the eye-opening statement.

This delicate situation presents the industry with the chance to build a more sustainable future for food. Traditional agriculture is a major contributor to global greenhouse gas emissions and other deleterious environmental impacts. With that in mind, for those investors thinking about stockpicking and ESG principles, the rise in meat alternatives offers some intriguing options.

Plant-based products

So far, apart from the standard vegan and vegetarian offerings which have been on the market for some years, it is plant-based products that have been at the forefront of the non-meat and alternative proteins push.

The aim is for such products to replicate the experience of eating meat. Fat, protein and all the usual things in meat are still in play – but are taken from plants. Proteins are used to mimic the blood that the meat eater would expect.

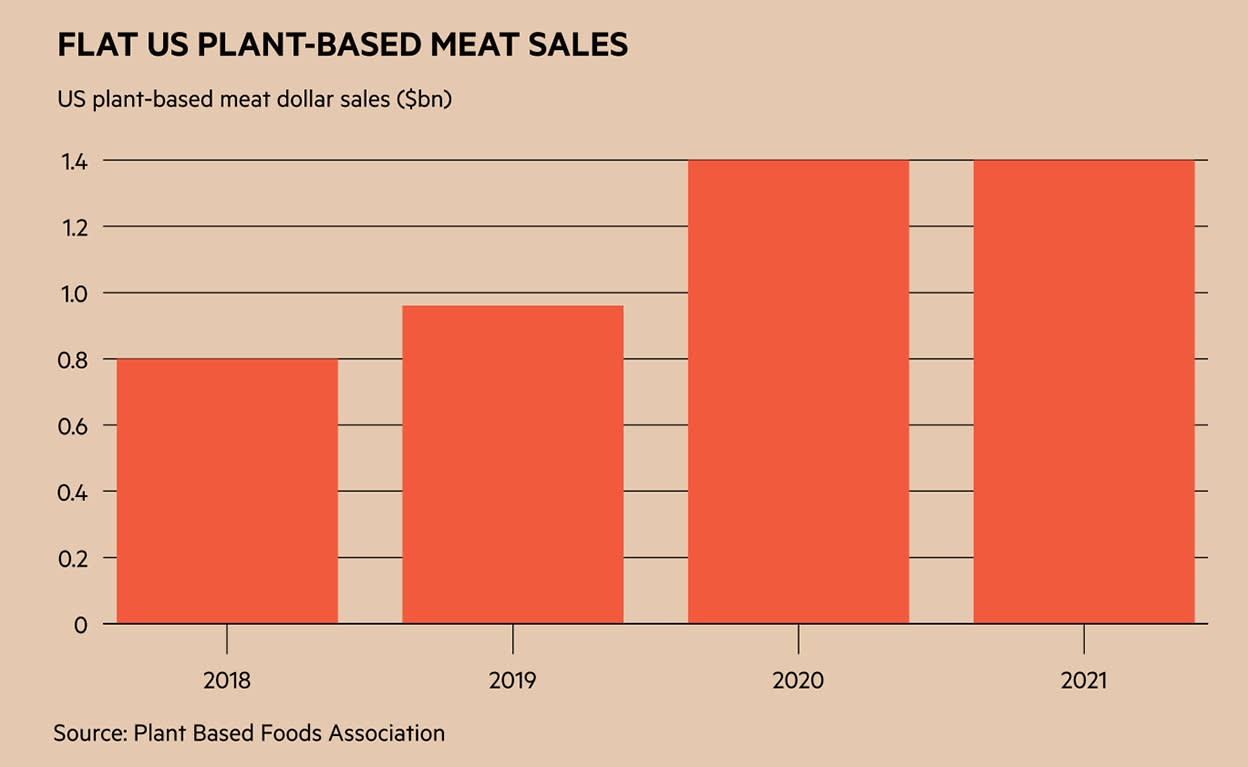

But there has been some disquiet in the plant-based meat world of late. After a boom in sales, things have come back down to earth. In the US, sales remained flat in 2021 at around $1.4bn, according to Plant Based Foods Association data. Still, revenues were up by 74 per cent on a three-year basis, unit sales growth outstripped the conventional meat market, and consumer demand rose. This is hardly disaster territory.

Beyond Meat (US:BYND), the US-based purveyor of products such as plant-based sausages and burgers, is a key player. Its performance is often seen as indicative of the wider market’s fortunes, and recent postings have got meat alternative bulls a bit nervy. Since listing in 2019, the company’s star has dimmed notably, with its share price collapsing by over 60 per cent. In its first quarter of 2022, the company posted net revenue growth of only 1.2 per cent, and its gross margin plummeted to just 0.2 per cent of net revenues, from over 30 per cent in the comparative period.

As is often common with transformative products and trends, hype and speculation have conspired to unmoor expectations from fundamentals. Nonetheless, analysts are closely watching for news of the long-expected IPO of the Bill Gates-backed Impossible Foods, rumoured to be worth up to $10bn, which has just launched products in the UK.

While it is still very early days for the sector, the growing profusion of products and companies mean that competition is already a big threat.

For along with our US cousins, UK-listed companies are also adapting to the plant-based foods trend. This includes several of the big beasts. Plant-based foods are “at the heart of” Unilever’s (ULVR) strategy, for example. The company is aiming to hit €1bn in annual sales from plant-based meat and dairy alternatives through brands such as The Vegetarian Butcher. In its latest trading update, the company pointed to its Knorr brand as “responding to consumer needs in fast-growing segments such as plant-based innovations in Latin America”. Analysts expect Unilever’s annual food and refreshment sales to be over €20bn in 2024, which makes the alternative foods target relatively small. But the company’s food performance has been lacklustre in recent times, meaning that growth in this area (which could pick up by more than expected) could have an outsized impact.

Hilton Food (HFG) has a target of doubling sales from plant-based, vegetarian and flexitarian products by 2025 (from a 2020 baseline). The business started life as a traditional meat producer, but has expanded to deal in alternative fare. Vegan and vegetarian volumes increased by more than a quarter between 2019 and 2021, and plant and fish products are performing well in European markets. The acquisition of Dutch manufacturer Dalco has given the company exposure to plant-based proteins, while the purchase of specialist salmon business Foppen has expanded its alternative proteins portfolio. Numis analysts said that the company “broadening its protein offering” is helping it to battle inflation.

There is also plenty of action when it comes to dairy alternatives. Soft drinks producer Britvic (BVIC), for example, acquired then relaunched Plenish last year – with major additional distribution for its plant-based milk and shots. It is hoped that March’s rebrand will help accelerate growth on this side of the business. The company posted 17 per cent revenue growth in its latest interim results and announced a £75mn share buyback programme.

New innovations

But there is more to the future of food than plant-based alternatives. Technological advancement is driving progress within the sector, and changing the face of the industry. Analysts see great growth potential in areas such as cultured meat and indoor farming, with the potential benefits being both economically and environmentally advantageous.

The idea behind cultured meat is the production of genuine meat without the need to farm and slaughter animals. A tissue sample is taken from an animal, with the cells then grown in a bioreactor. The cells differentiate into muscle, fat, etc, and can then be produced into the final product. While the bioreactor process is energy-intensive, cultured meat is forecast to be significantly less harmful than conventional farming when it comes to energy, emissions, water and land use.

BoA analyst Felix Tran told Investors’ Chronicle that such advancements will fundamentally change the industry. In the long-term, “cultured meat has the ability to scale up and has big disruption potential” he said.

The authors of a recent report by Kearney, the consultancy, wrote that “novel vegan meat replacements are expected to be most relevant during the long-term transition toward cultured meat, but cultured meat is predicted to triumph thanks to its fusion of sustainability and tailor-made nutrition, which should satisfy a diverse range of customers”.

While much of the activity in the cultured meat area is currently going on within private companies, there are quoted businesses available for private investors. BSF Enterprise (BSFA) has just listed in London. It owns 3D Bio-Tissues Limited, a tissue engineering business, which is focused on “producing the UK’s first 100 per cent lab-grown meat in the next 12 months”. We watch with interest.

We have previously flagged Agronomics (ANIC) as an option for investors interested in the cultured meat sector. This remains the case. The Aim-traded company deals in the field of cellular agriculture, and its portfolio of venture-stage companies are involved in the sector. Its investments include cultured meat firms Mosa Meat (Dutch) and chicken-focused SuperMeat (Israeli). The shares are currently trading on a consensus 15 times forward earnings.

Indoor, also referred to as ‘vertical’, farming, is another important development. Crops are grown in controlled conditions using LED lighting and without the use of pesticides (since the farms are indoors). These farms can produce hundreds of times more yield than standard outdoor farms – although operators are currently struggling with high energy costs.

In the UK market, BoA is particularly keen on Ocado (OCDO) in the future food space. Ocado has a controlling interest in Jones Food Company, “the UK’s leading vertical farming company”, which raised £25mn in April to build a second vertical farm near Bristol. We are bearish on lossmaking Ocado based on its high net debt, climbing capital costs, and tough competition. But the vertical farming part of the business is something to watch, especially considering that Credit Suisse thinks that the technology could potentially meet 80 per cent of urban food demand in the future.

BoA’s Tran also pointed across the Irish Sea to nutrition businesses Kerry Group (IE:KRZ) and Glanbia (IE:GL9) as stocks the bank thinks could benefit from the general alternative meat trend. The companies are trading on a consensus 22 times and 12 times forward earnings, respectively.

One way of keeping up with innovation is to see which companies are ramping up capital expenditure (capex) and research and development spending. Shore Capital analysts said that the average capex spend as a portion of sales for UK food companies over the past five years came in at 3.9 per cent. Britvic, Cranswick, Devro and Treatt all spent more than this in their latest respective financial years – Treatt came out on top with 12 per cent of sales spent on capex.

Brexit opportunities?

As well as labour shortages, food exporters are also dealing with increased red tape as a result of Brexit. But leaving the EU also offers the UK the chance to differentiate itself from Europe in a positive way.

Enter the Genetic Technology (Precision Breeding) Bill, which was introduced in Parliament on 25 May and which the government hopes will land on the statute book this year. The legislation will apply to England only, although products may also be sold in Scotland and Wales, and opens the door to gene-edited food.

The legislation “will remove unnecessary barriers to research into new gene editing technology, which for too long has been held back by the EU’s rules around gene editing, which focus on legal interpretation rather than science – hindering the UK’s world leading agricultural research institutions” said the Department for Environment, Food and Rural Affairs.

Under EU guidelines, the UK was unable to exploit gene-edited food due to there being no distinction made between genome-edited crops and genetic modification of organisms – both were de facto outlawed. In a well-timed coincidence, just days before the bill’s introduction to parliament, UK scientists created vitamin-D-heavy tomatoes using gene editing technology, which provides a germane example of the possibilities.

Another policy paper is keenly awaited. The upcoming government white paper setting out a new ‘national food strategy’ will give further detail on the executive’s approach to the legislative future of the sector. This is expected to be released shortly, and comes in response to an independent review led by businessman Henry Dimbleby.

There are hopes within the industry that the paper could open up the way to UK success in cultured meat production, again by diverging from Europe and offering a distinct regulatory and investment proposition.

Of course, we are at an early stage when it comes to funding, regulation and technology around these developments. While gene-edited crops and cultured meat could make great ESG plays for investors, there is still much work to be done on pricing (for example) – although the cultured meat industry is adamant that costs will come down and will ultimately be comparable with standard meat products.

What next for meaty companies?

Where do these trends leave traditional agriculture companies and those focused on meat? Looking a bit exposed. While meat consumption at a global level is set to rise, there is the sense that simply sticking to business as usual won’t cut it any more. BoA thinks that “the long-term losers will be excessive fertiliser use, legacy rural agriculture and traditional animal production farming”.

Sausage caser Devro is an obvious example. The company told Investors’ Chronicle that non-meat sausages are forecast to grow from around 1 per cent to 3 per cent of the total market, which represents “significant growth” and said that its own proposition “now includes looking beyond collagen and pursuing potential technologies that can be applied in non-meat-based products” in acknowledgement of this. Cranswick, meanwhile, boosted its alternative foods offering with last year’s acquisition of Ramona Kitchens, a supplier of Mediterranean plant-based foods. Mediterranean foods posted the best revenue growth by category in the company’s latest annual results, up by 24.3 per cent.

Devro and Cranswick’s actions hammer home the importance of diversification. This principle applies to both the traditional meat industry and to the disruptors, as Beyond Meat’s performance has shown. In the short term at least, going fully meat or fully alternative may not be the best solution for companies – as the popularity of the flexitarian diet demonstrates, there is a diverse customer base to satisfy.

So, the move towards plant-based meats and similar alternatives isn’t a simple panacea for corporate growth and shareholder returns. Far from it. But the trends and technologies that underpin the future of the food sector mean that it will look very different over the decades to come. And companies, as well as investors, need to be prepared.

| Some UK-listed foody options | |||||||||

|---|---|---|---|---|---|---|---|---|---|

| Company name | Ticker | Price (£) | Price change 1-yr (%) | Price change 5-yr (%) | Fwd Sales Growth (%) | PE | Dividend Yield (DY) | EV/EBITDA | Market cap (£ Mn) |

| Agronomics | ANIC-GB | 0.19 | -19.8 | 223.4 | 54.4 | 30 | nil | 92.0 | 186 |

| Britvic | BVIC-GB | 8.30 | -9.1 | 18.1 | 12.0 | 19 | 2.7 | 12.1 | 2,215 |

| Cranswick | CWK-GB | 30.7 | -22.5 | 4.1 | 7.1 | 16 | 1.9 | 10.2 | 1,628 |

| Devro | DVO-GB | 2.09 | 0.2 | -3.0 | 5.2 | 11 | 4.5 | 6.66 | 352 |

| Hilton Food Group | HFG-GB | 11.1 | -6.7 | 45.0 | 11.5 | 25 | 2.6 | 9.51 | 1,000 |

| Treatt | TET-GB | 9.00 | -21.7 | 95.7 | 14.9 | 35 | 0.7 | 26.8 | 496 |

| Unilever PLC | ULVR-GB | 35.0 | -17.3 | -18.9 | 11.2 | 17 | 4.6 | 12.9 | 88,696 |

| Source: FactSet | |||||||||

Source: investorschronicle.co.uk