Citigroup (C) recently renewed its outlook on two mega-cap stocks, namely Tesla (TSLA) and Micron (MU). The investment firm slashed Micron’s revenue forecast but maintained its buy rating. In addition, Citigroup provided an update on Tesla in which it receded its earnings estimate based on inactivity in China.

I foresee two opposing destinies for Micron and Tesla. I’m bullish on Micron but Bearish on Tesla, as I believe they’ll be uniquely affected by the economic cycle; here’s why.

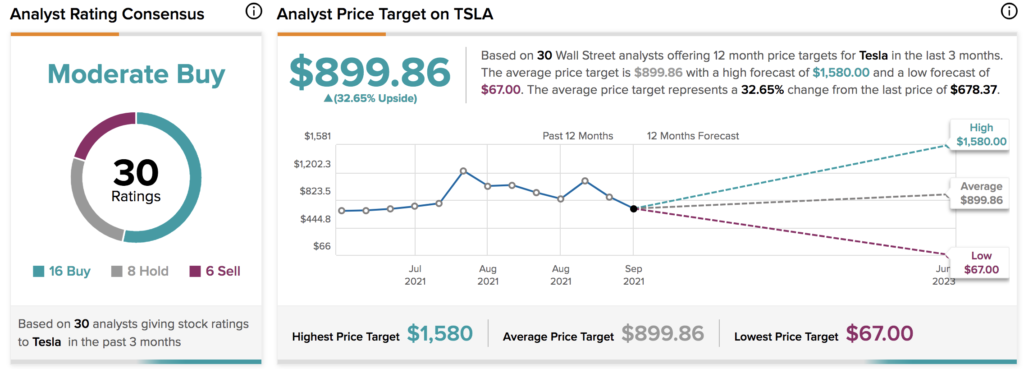

Tesla

Itay Michaeli cut Tesla’s earnings outlook ahead of the firm’s second-quarter deliveries update. The analyst cut his Tesla earnings-per-share target by 2% amid disruptions in Shanghai and rising input costs.

It’s trivial that Tesla could fall victim to the current economic environment. In fact, the yield curve spells it all out for us. The yield curve implies that U.S. interest rates could settle above 3% within the next two years. If rates had to rise that high, we could see a contraction in durable goods sales as there’s an overwhelming amount of financial literature that concludes a negative correlation between durable goods sales and interest rates. In addition, rising interest rates will likely suppress the global consumer base’s borrowing capacity, which could adversely affect electronic vehicle sales.

Further to the possible economic growth woes argument is Tesla’s worrisome valuation metrics. Tesla stock is trading at 11.27x sales and 52.23x cash flow. Relative valuation metrics usually don’t provide much help in growth stock price discovery. However, considering the economic cycle and the nature of Tesla’s products, it’s safe to say that most investors will be concerned with its top-line multiples being as high as they are.

The final factor to consider with Tesla’s near-term price outlook is its momentum profile. The stock’s trading below its 50-, 100-, and 200-day moving averages at a midrange RSI (Relative Strength Index) of 46.58. This conveys that Tesla will need a catalyst to reverse its more than 40% year-to-date price drop, which is unlikely in the current economic climate.

Turning to Wall Street, Tesla earns a Moderate Buy consensus rating based on 16 Buys, eight Holds, and six Sell ratings assigned in the past three months. The average TSLA stock price target of $899.86 implies 32.65% upside potential.

Micron

In his Micron stock analysis, Christopher Danely of Citigroup noted: “We are lowering our estimates again but reiterate our Buy rating on [Micron] due to attractive valuation and secularly increasing fundamentals through cycles.”

Danely’s reference to secular growth is of the essence. Micron could erupt as a winner, even during a bear market, as secular growth stocks don’t exhibit sensitivity to economic cycles. Its compound annual growth (CAGR) rates convey the company’s secular attributes. For example, Micron’s 5-year EBITDA CAGR of 29.77% suggests that the firm’s growing much faster than the broader economy.

Furthermore, Micron possesses solid industry positioning. The firm holds down approximately 17.49% in broad-based market shares across its business verticals, implying that it has the capacity to price its products competitively and bargain with its suppliers. Moreover, Micron operates at economies of scale with a 45.97% gross profit margin, which means it’s leveraging its size to operate efficiently.

Micron’s robust growth means that its stock’s behavior could be independent of the yield curve. As explained earlier, the yield curve’s rise compresses the spending power of consumers, which causes cyclical stocks to deteriorate. However, demand exceeds supply in the semiconductor space, which is visible in Micron’s key growth metrics. Thus, a prolonged bear market probably won’t have the same effect on Micron as it would on the broader stock universe.

Lastly, the stock’s undervalued on a normalized basis. Micron’s price-earnings and price-cash flow ratios are at discounts worth 42.57% and 18.43%, respectively. In addition, Micron’s PEG ratio of 0.04x hints that investors underscore the stock’s earnings-per-share growth potential.

Turning to Wall Street, Micron earns a Moderate Buy consensus rating based on 15 Buys, three Holds, and one Sell rating assigned in the past three months. The average MU stock price target of $93.93 implies 66.51% upside potential.

Concluding Thoughts

Tesla and Micron are under the microscope after Citigroup slashed both firms’ growth prospects. However, key metrics and economic variables imply that Micron could dodge any economic headwinds, while Tesla will likely exhibit excess sensitivity to the same variables.

Read full Disclosure

Source: tipranks.com