CreativeNature_nl/iStock via Getty Images

Welcome to the October 2022 edition of the lithium miner news. The past month saw a very strong lead from the U.S government with $2.8 billion of grants awarded to help supercharge U.S. manufacturing of batteries for electric vehicles and the electric grid. This boosted sentiment in the lithium sector despite the poor macro-economic conditions. Chinese lithium producers issued positive profit alerts and China EV sales continued with record results.

Lithium price news

Asian Metal reported during the past 30 days, the 99.5% China lithium carbonate spot price was up 6.05% and the China lithium hydroxide price was up 5.68%. The Lithium Iron Phosphate (Li 3.9% min) price was up 3.33%. The Spodumene (6% min) price was up 4.53% over the past 30 days.

Benchmark Mineral Intelligence reported lithium prices of (battery grade carbonate – RMB 529,000 ($73,525), hydroxide RMB 524,000 ($72,825), and Benchmark stated (paywalled): “In addition to robust demand growth from the EV industry, contacts reported to Benchmark that burgeoning demand from the energy storage sector in recent months has also acted to fill several lithium producers order books until 2023, placing upward price pressure on the lithium chemicals market.”

Metal.com reported lithium spodumene concentrate (6%, CIF China) price of CNY 37,870 (~USD 5,227/mt), as of October 21, 2022.

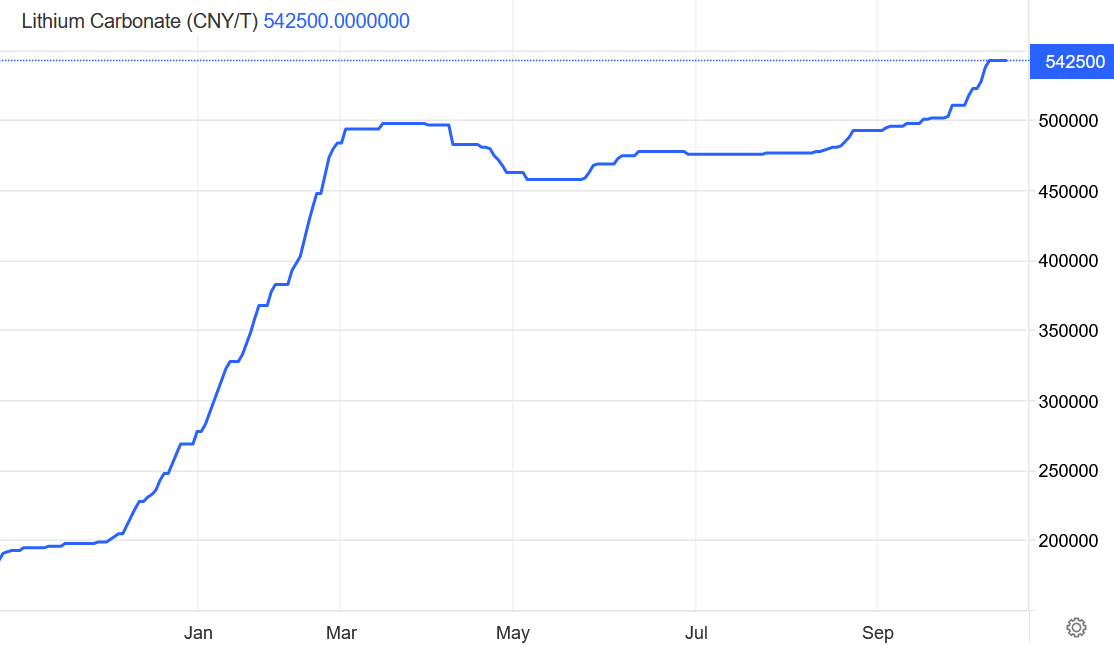

China Lithium carbonate spot price – CNY 542,500 (~USD 74,891)

Trading Economics

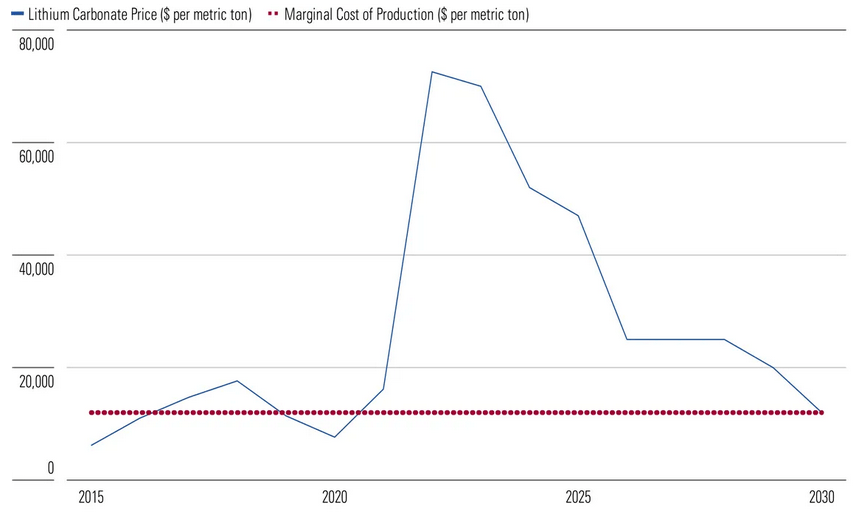

Morningstar’s lithium price forecast 2022 to 2030 (as of mid 2022)

Morningstar

Lithium demand versus supply outlook

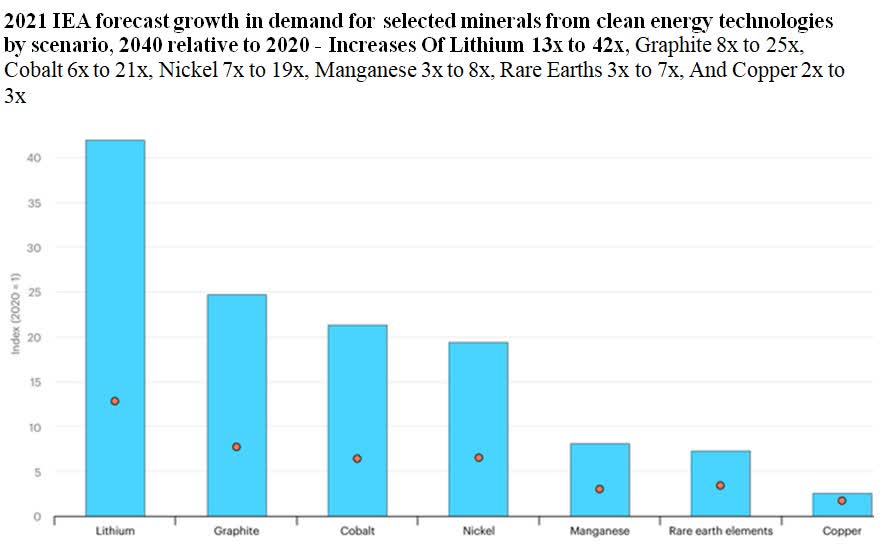

2021 IEA forecast growth in demand for selected minerals from clean energy technologies by scenario, 2040 relative to 2020 – Increases Of Lithium 13x to 42x, Graphite 8x to 25x, Cobalt 6x to 21x, Nickel 7x to 19x, Manganese 3x to 8x, Rare Earths 3x to 7x, And Copper 2x to 3x

IEA

UBS’s EV metals demand forecast (from Nov. 2020)

UBS

Rio Tinto forecasts lithium emerging supply gap (October 2021) – 60 new mines the size of Jadar will be needed

Rio Tinto

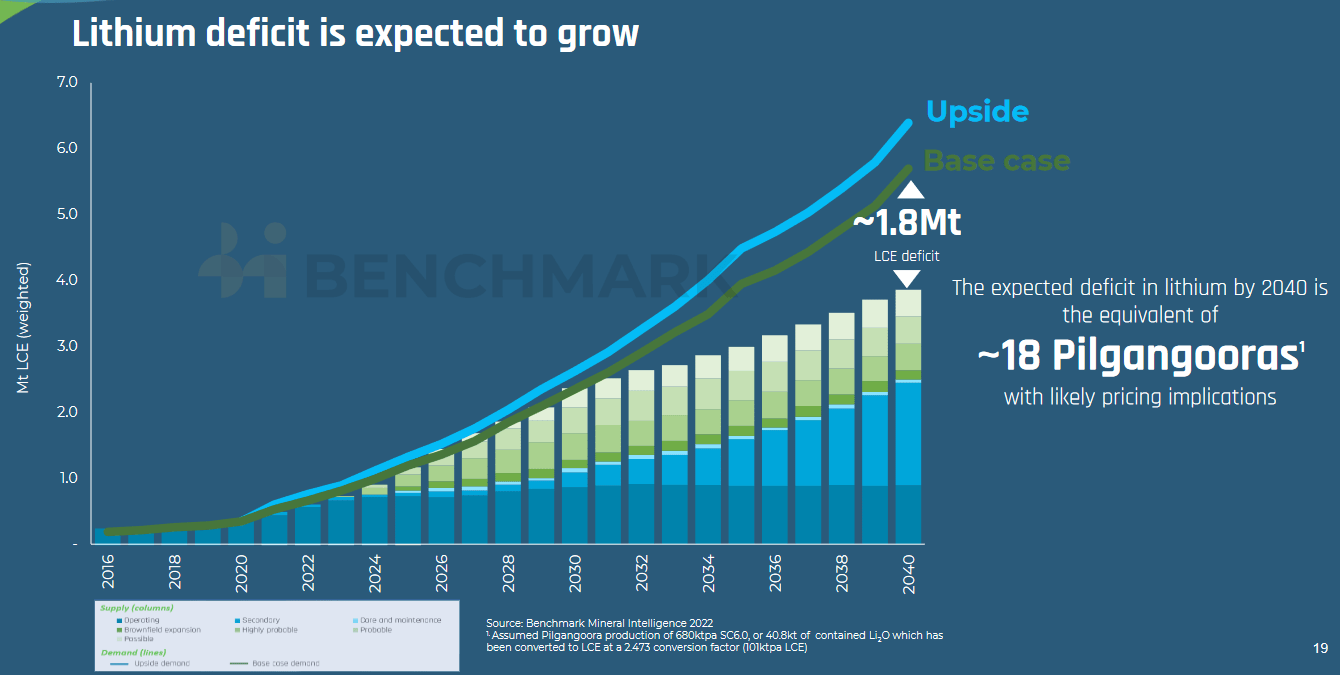

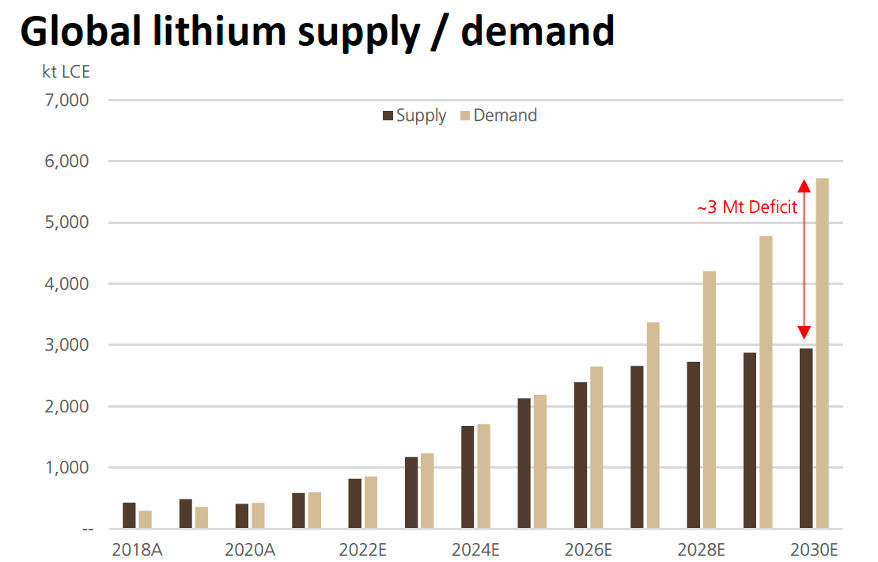

Lithium demand v supply forecast by Benchmark Mineral Intelligence (from mid 2022)

BMI

BMI (2021 forecast) – If supply can be rapidly ramped in future years it can come close to meeting surging demand

BMI

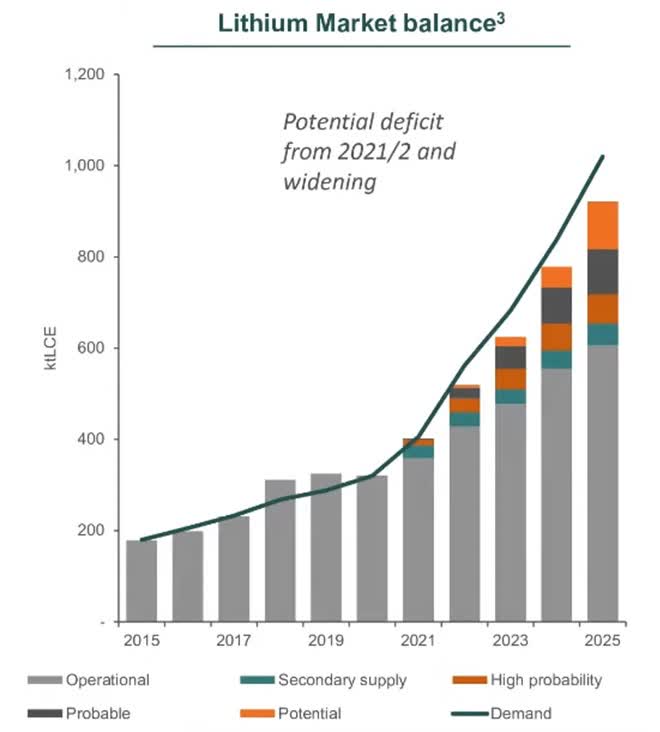

UBS forecasts Year battery metals go into deficit (chart from 2021) – Source: UBS courtesy Carlos Vincens LinkedIn

UBS

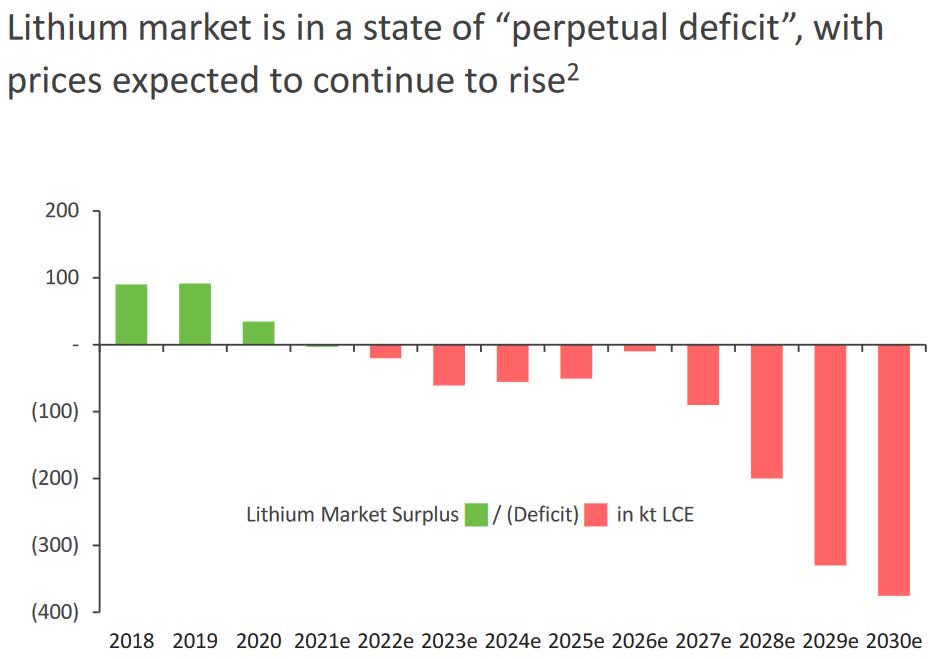

Macquarie’s lithium demand v supply forecast (July 2021) – Deficits from 2022 growing bigger from 2027

Macquarie

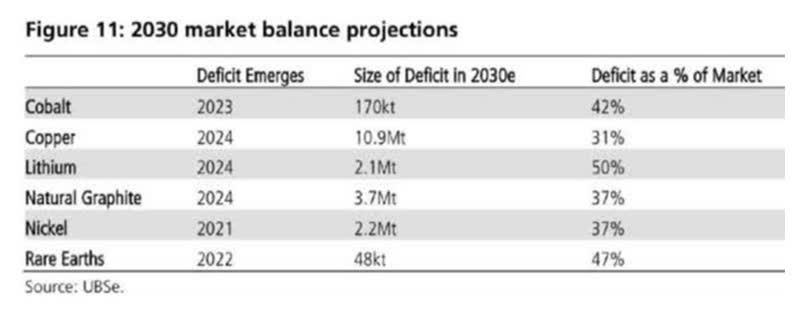

2022 – UBS lithium demand v supply forecast to 2030

UBS

BloombergNEF lithium demand v supply forecast (as of mid 2022)

BloombergNEF

BMI – Global lithium-ion battery gigafactory pipeline – now at 304 and 6,387.6 GWh as of May 2022

BMI

BMI

BMI

BMI forecasts Li-ion battery cell capacity to grow at a CAGR of 47% from 2021 to 2032 (as of mid 2022)

BMI

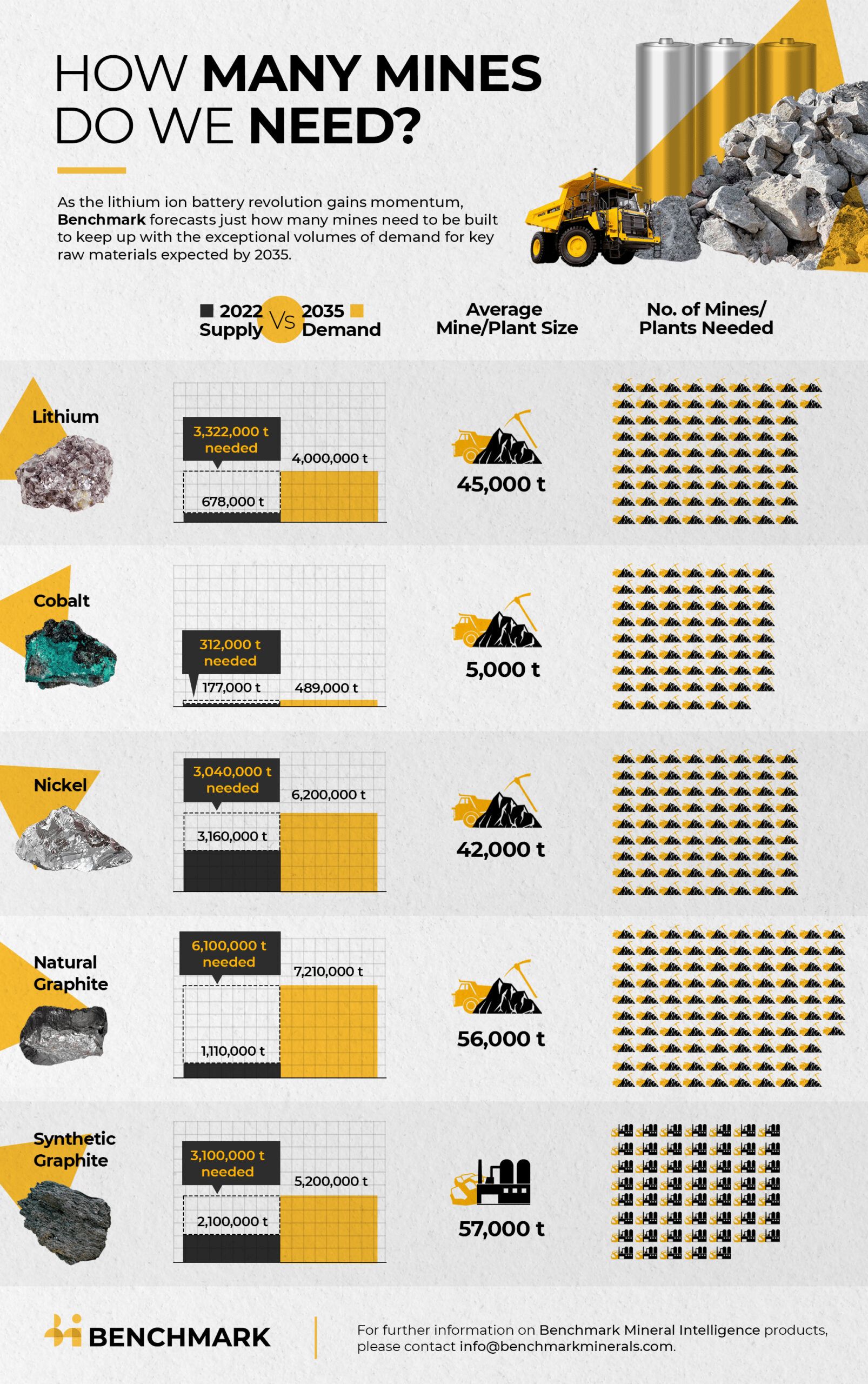

2022 – BMI forecasts we need 330+ new EV metal mines from 2022 to 2035 to meet surging demand – 74 new 45,000tpa LCE lithium mines (59 if include recycling)

BMI

Lithium market and battery news

On September 26 Reuters reported:

Volkswagen teams up with Umicore on battery materials.

- Volkswagen’s PowerCo in 3 bln euro JV with Umicore

- JV to produce battery cathodes, probably in Poland

- European automakers seek supply chains closer to home

On September 27 Mining.com reported:

Rio Tinto warns miners not moving fast enough on lithium extraction… Planned lithium production will fail to meet growth in demand for lithium-ion batteries that are needed to meet global climate goals, according to Rio Tinto Plc’s minerals chief. Lithium consumption needed “to surge way above anything that’s planned to be mined”…

On September 28 BNN Bloomberg reported: “CATL plans $1.9 billion battery project in China’s Luoyang City.”

On October 4 Mining.com reported:

Australia could grab 20% of the world’s lithium refining by 2027… If these plans progress on time Australia could have 10% of the refining market by 2024 from a negligible amount currently, and 20% by 2027, the government said in a report released Tuesday.

On October 5 EnergyWire reported:

U.S. shift on child labor may scramble EV sector… The Biden administration declared Tuesday that batteries from China may be tainted by child labor… The Department of Labor said it would add lithium-ion batteries to a list of goods made with materials known to be produced with child or forced labor under a 2006 human trafficking law… Dummett said his concern lies in what he views as a toothless approach from the department. Unlike the full ban against solar panels from Xinjiang, the U.S. government list exists primarily for informational purposes and is “not intended to be punitive,” according to the department.

On October 10 Seeking Alpha reported:

FREYR Battery signs license and services agreement with Aleees to produce active cathode material… The agreement includes ongoing services and support from Aleees, provides FREYR with a worldwide license to produce and sell LFP cathode material based on Aleees’ technology, and to build production facilities leveraging Aleees’ industrial expertise. The company anticipates that the agreement will enable it to meet the future LFP cathode material needs of the Giga Arctic battery production facility in Mo i Rana, Norway and volumes could furthermore be deployed to the company’s planned Giga America project in the U.S.

On October 12 CleanTechnica reported:

NASA solid-state battery is lighter & more powerful. NASA says it has created a novel solid state battery that has enough energy and power to be used in electric airplanes and other aeronautical devices.

On October 13 Seeking Alpha reported:

Albemarle downgraded as Berenberg, Morgan Stanley predict lithium price drop… Morgan Stanley predicted a “large fall” in lithium exports and prices from Sociedad Química y Minera (NYSE:SQM), citing September data that showed a 10% decline in SQM’s volumes and an 11% drop in prices from August. SQM told Morgan Stanley it still expects to see flat prices in H2 2022, so the September price and volume decline could just be an anomaly…

On October 13 Market Index reported:

Lithium stocks tumble after Morgan Stanley flags fall in both price and exports… Supply tight narrative still intact… “Recent Lithium price peak had a clear implicit message: demand is strong and inventories are tight,” said the analysts. “Although we have mapped some amounts of new supply, we expect the market to remain tight through 2022, especially when considering restocking needs.” “We still expect lithium prices to trend lower in 2023, as supply expands and market tightness eases.”

On October 13 Benchmark Mineral Intelligence announced:

Lithium has to scale twenty times by 2050 as automakers face generational challenge. The world will need more than twenty times the amount of lithium than was mined last year to meet demand by mid-century, according to new data from Benchmark Mineral Intelligence, driven by growth in energy storage and electric vehicles.

On October 14 The Financial Post reported:

Canada will fast-track energy and mining projects important to allies: Freeland… Canada will have to fast-track energy and mining projects if it is to help its democratic allies and achieve its own net-zero ambitions, Deputy Prime Minister Chrystia Freeland said in a speech this week in Washington… Freeland also addressed calls for the federal government to create incentives to decarbonize on par with those in the U.S. Inflation Reduction Act – legislation that could prompt a surge in investment in emissions reduction and renewables south of the border over the next decade.

On October 19 CNBC reported:

“Elon Musk addresses Twitter takeover, possible recession on Tesla earnings call. “Tesla wrote, in its shareholder deck, “We continue to believe that battery supply chain constraints will be the main limiting factor to EV market growth in the medium and long terms.”

Note: Bold emphasis by the author.

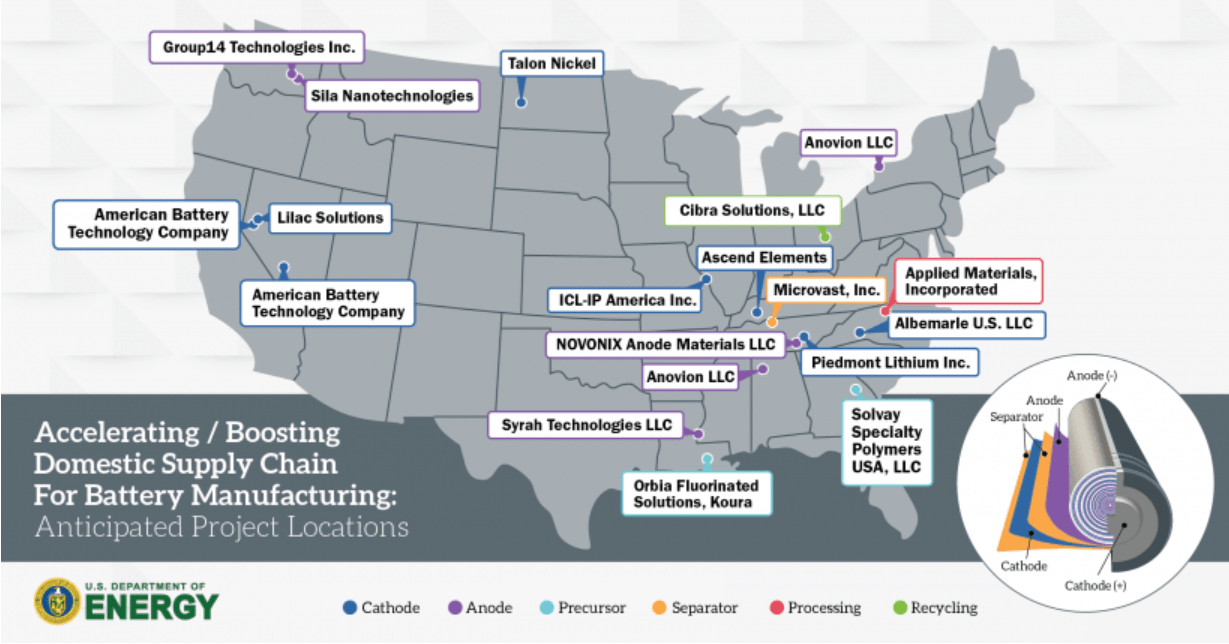

On October 19 the White House released:

Bipartisan Infrastructure Law: Battery Materials Processing and Battery Manufacturing Recycling Selections | Department of Energy. Funded with $2.8 billion through the Bipartisan Infrastructure Law, the portfolio of 21 projects supports new, retrofitted, and expanded commercial-scale domestic facilities to produce battery materials, processing, and battery recycling and manufacturing demonstrations.

Location map showing the planned project locations of the DoE 21 project grant recipients – Albemarle & Piedmont Lithium were lithium related winners

DoE

Also on October 19 Energy.Gov announced:

Biden-Harris administration awards $2.8 Billion to supercharge U.S. manufacturing of batteries for electric vehicles and electric grid. The 20 companies will receive a combined $2.8 billion to build and expand commercial-scale facilities in 12 states to extract and process lithium, graphite and other battery materials, manufacture components, and demonstrate new approaches, including manufacturing components from recycled materials. The Federal investment will be matched by recipients to leverage a total of more than $9 billion to boost American production of clean energy technology, create good-paying jobs, and support President Biden’s national goals for electric vehicles to make up half of all new vehicle sales by 2030 and to transition to a net-zero emissions economy by 2050… DOE anticipates moving quickly on additional funding opportunities to continue to fill gaps in and strengthen the domestic battery supply chain… The President also announced the launch of the American Battery Material Initiative… The Initiative will coordinate domestic and international efforts to accelerate permitting for critical minerals projects, ensuring that the United States develops the resources the country needs in an efficient and timely manner, while strengthening Tribal consultation, community engagement, and environmental standards to build smarter, faster, and fairer.

Lithium miner news

Albemarle (NYSE:ALB)

On October 19, Albemarle announced:

Albemarle secures DOE grant for U.S.-based lithium facility to support domestic EV supply chain… has been awarded a nearly $150 million grant from the U.S. Department of Energy (DOE)… The grant funding is intended to support a portion of the anticipated cost to construct a new, commercial-scale U.S.-based lithium concentrator facility at Albemarle’s Kings Mountain, North Carolina, location. Albemarle expects the concentrator facility to create hundreds of construction and full-time jobs, and to supply up to 350,000 metric tons per year of spodumene concentrate to the company’s previously announced mega-flex lithium conversion facility. The mega-flex conversion facility is expected to eventually produce up to 100,000 metric tons of battery-grade lithium per year to support domestic manufacturing of up to 1.6 million EVs per year. Albemarle is finalizing the site selection for the mega-flex conversion facility in the southeastern United States…

Note: More details here.

Upcoming catalysts:

- Q3 2022 – Wodgina Lithium Mine (60% ALB: 40% MIN) Train 2 restart. Note the non-binding agreement will (if completes) move Wodgina to a 50% ALB: 50% MIN JV.

NB: The Greenbushes Mine in WA is owned by Albemarle 49%, Tianqi Lithium Corporation ~25%, and IGO Limited ~25%. Wodgina Lithium Mine is a JV (50% ALB: 50% MIN). Kemerton Lithium Hydroxide Plant is a JV (60% ALB: 40% MIN).

Kemerton Lithium Hydroxide Plant (60% ALB: 40% MIN) in WA

Albemarle

Sociedad Quimica y Minera S.A. (NYSE:SQM), Wesfarmers [ASX:WES] (OTCPK:WFAFY), Covalent Lithium (SQM/WES JV)

No lithium news for the month.

Upcoming catalysts:

Q4, 2023 – Mt Holland spodumene production to begin (SQM/Wesfarmers JV).

Q4, 2024 – 50ktpa Lithium hydroxide [LiOH] refinery (SQM/Wesfarmers JV).

Investors can read SQM’s latest presentation here or the latest Trend Investing article on SQM here.

Jiangxi Ganfeng Lithium [SHE:002460] [HK: 1772] (OTCPK:GNENF) (OTCPK:GNENY)

On October 13, Energy Trend reported:

Ganfeng will invest another RMB 30 billion in Yichun, Asia’s lithium capital. Major Chinese lithium supplier Ganfeng Lithium maintains an aggressive pace in its investment activities. On September 28, it disclosed that it has signed a new strategic cooperation agreement with the government of Yichun for the joint development of a project that encompasses lithium resources, Li-ion battery materials, new types of Li-ion batteries, and products for various energy storage applications. Ganfeng signed this agreement just after it had announced a capital injection of more than RMB 6 billion into GFL International and Jiangxi Lingneng Lithium Industry. Yichun is a city in China’s Jiangxi Province.

On October 17, Gasgoo reported:

Ganfeng Lithium’s Q1-Q3 2022 net profit projected to soar 478.29%-518.73% YoY. Jiangxi Ganfeng Lithium Co., Ltd. (“Ganfeng Lithium”), one of the world’s leading producers of battery-grade lithium, announced on Oct. 15 that its net profit attributable to shareholders were estimated to be between 14.3 billion yuan ($1.986 billion) and 15.3 billion yuan ($2.125 billion) for the first three quarters of 2022 (Q1-Q3 2022), soaring 478.29%-518.73% year on year. Excluding the impact of certain non-recurring gains and losses, the company expects its Q1-Q3 net profit to rocket 831.45%-901.48% from a year earlier to 13.3 billion-14.3 billion yuan ($1.847 billion-$1.986 billion).

Investors can read the latest Trend Investing article on Ganfeng Lithium here.

(Chengdu) Tianqi Lithium Industries Inc. [SHE:002466], Tianqi Lithium Energy Australia (TLEA) is a JV with Tianqi Lithium (51%) and IGO Limited (49%). TLEA owns the Kwinana lithium hydroxide facility in WA

On October 14, Tianqi Lithium announced:

Positive profit alert… for the nine months ended September30, 2022, (i) the net profit attributable to the shareholders of the Company would range from RMB15,200 million to RMB16,900 million representing an increase of approximately 2,768.96% to 3,089.83% as compared with that of approximately RMB529,809,500 for the corresponding period of last year…

You can watch a good Tainqi lithium CEO video interview here, where he discusses lithium market demand and supply issues.

Kwinana lithium refinery JV (51% Tianqi: 49% IGO) in Western Australia

IGO Limited

Pilbara Minerals [ASX:PLS] (OTC:PILBF)

On October 13, Pilbara Minerals announced: “2022 annual report.”

On October 18, Pilbara Minerals announced:

BMX pre-auction bid ~US$7,830/DMT… A shipment of 5,000dmt on a 5.5% lithia basis was made available for sale to the group of registered BMX participants prior to the proposed BMX auction scheduled for Tuesday, 18 October 2022. The Company is pleased with the strong responses received from participants and has accepted a pre-auction offer of US$7,100/dmt (SC5.5, FOB Port Hedland basis) with a 10% deposit due shortly. This offer of US$7,100/dmt equates to an approximate price of US$7,830/dmt on a SC6.0 CIF China equivalent basis after adjusting for lithia content on a pro rata basis and freight costs. Shipment is expected from mid-November.

On October 24 Pilbara Minerals announced:

Additional cargo sale ~US$8,000/dmt… advise that it has entered into a further contract of sale for an additional 5,000dmt cargo following completion of the BMX pre-auction sale process undertaken and announced on Tuesday 18 October. The Company has entered into a sale contract for 5,000dmt SC5.5 FOB Port Hedland priced at US$7,255/dmt which is the equivalent of ~US$8,000/dmt on an SC6.0 CIF China basis after adjusting for lithia content on a pro-rata basis and inclusive of freight costs.

Upcoming catalysts:

Late 2023 – Plan to commission production of POSCO/Pilbara Minerals (18%, option to increase to 30%) JV LiOH facility in Korea.

Mineral Resources [ASX:MIN] (OTCPK:MALRF)

Mt Marion Mine (50% MIN: 50% Ganfeng). Wodgina Lithium Mine (60% ALB: 40% MIN) restarted in mid 2022. (Note the non-binding agreement will (if completes) move Wodgina to a 50% ALB: 50% MIN JV). The 50ktpa Kemerton Lithium Hydroxide refinery (60% ALB: 40% MIN) is due for first sales in H2, 2022.

On October 7, Mineral Resources announced: “Lithium Mineral Resources and reserve update.” Highlights include:

- “Wodgina Indicated & Inferred Mineral Resources estimated at 259.2 Mt at 1.17% Li2O.

- Wodgina Ore Reserve estimated at 147.0 Mt at 1.20% Li2O.

- Mt Marion Indicated & Inferred Mineral Resources estimated at 51.4 Mt at 1.45% Li2O.

- Maiden Mt Marion Ore Reserve estimated at 17.2 Mt at 1.56% Li2O.”

On October 11 Market Index reported:

MinRes rallies as the lithium hydroxide plant strategy evolves. Mineral Resources believes it can build a 50,000 tonne a year lithium hydroxide plant in WA for US$650m. MinRes is targeting 120,000 tonnes a year of lithium carbonate equivalent (LCE) production from the Wodgina and Mt Marion mines in the next five years. Goldman Sachs is Buy rated on MinRes with a price target of $76… The company could opt for a $10bn-plus demerger of the business while retaining its mining services and iron ore divisions. It’s understood JPMorgan has been assessing potential spin-off structures, and a potential US listing for the lithium business and Albemarle has previously hinted that it could be a future acquirer… Management notes progress at Wodgina is proceeding well, with trains 1 to 3 potentially operating at 25% above nameplate capacity and produce 900,000-950,000 tonnes a year of spodumene for conversion into hydroxide. Study work is now advanced on train 4 which will likely be larger than the existing trains, producing potentially up to 500ktpa of spodumene, with approval likely in first half of 2023 and ramp-up sometime mid to late 2024.

On October 14, Mineral Resources announced: “2022 sustainability report.”

Investors can read the latest Trend Investing article on Mineral Resources here.

Livent Corp. (LTHM)[GR:8LV]

No news for the month.

You can read the Trend Investing Livent article here when Livent was trading at US$7.26.

Allkem [ASX:AKE] [TSX:AKE] (OTCPK:OROCF)(formerly Orocobre)

On October 5, Allkem announced: “Mt Cattlin resource drilling update.” Highlights include:

- “Phase 1 drilling is targeting to convert 3.2Mt of Resource to Reserves. Intercepts within this pit include high grade zones with large thicknesses such as 12m at 2.46% Li2O and 15m at 1.91% Li2O.

- Phase 2 drilling and assay results demonstrate resource extension potential to the north of the current pit with high grade intercepts in the lower pegmatite, including 9m at 2.98% Li2O and 7m at 1.86% Li2O…

- Mt Cattlin’s Mineral Resource tonnage recently increased 21% to 13.3Mt @ 1.2% Li2O and 131 ppm Ta2O5.”

On October 7, Allkem announced: “US$200m IFC project finance proposal for Sal de Vida.” Highlights include:

- “IFC has proposed a US$200 million project finance facility to support Allkem’s development of Sal de Vida Stage 1.

- IFC’s environmental and social performance requirements are globally recognised and will complement the ESG standards already adopted at Sal de Vida by Allkem.

- Subject to finalisation of commercial terms and other key outstanding items including final Board approval by both IFC and Allkem, the facility is expected to reach financial close by late CY22.”

On October 21, Allkem announced: “September 2022 quarterly activities report.” Highlights include:

Operations

- “Production at the Olaroz Lithium Facility2 was up 17% on the previous corresponding period (“PCP”) to 3,289 tonnes of lithium carbonate, 43% of which was battery grade material.

- Lithium carbonate sales were 3,721 tonnes, generating record quarterly revenue of ~US$150 million with a gross cash margin of 89%. Excluding shipments to Naraha, third party sales for the quarter averaged US$43,237/tonne3 FOB.

- The weighted average price for third party sales of lithium carbonate products in Q2 FY23 is expected to be approximately US$50,000/t FOB, 15% higher than the September quarter.

- In the September quarter, Mt Cattlin produced 17,606 dmt of spodumene and shipped 21,215 dmt, generating revenue of US$106.7 million4 with a gross cash margin of 80% based on an average sales price of US$5,028/dmt CIF for SC 5.4%. Cost of production was US$796/dmt FOB. An additional US$35 million of revenue was generated from sales of 59,326 dmt of low grade spodumene concentrate from pre-existing stockpiles and processing of fine-grained spodumene ore.

- Customer demand in the spodumene market remains robust and spodumene concentrate pricing in the December quarter is expected to be in line with the September quarter.”

Development Projects

- “Olaroz Stage 2 reached 93% completion… Mechanical completion, first production and ramp up is now planned for Q2 CY23…

- At Naraha, plant commissioning activities are well advanced with first production still expected during the December quarter.

- The first four ponds at Sal de Vida (“SDV”) Stage 1 are complete and are currently being filled with brine. Construction of the first two strings of ponds has reached 65% completion.

- At James Bay the clarification process for the ESIA with the Joint-Assessment Committee (Cree Nation and Federal government) concluded, a draft ESIA report was published and the final public consultation period has commenced with completion of the process anticipated by mid-November.

- Capital expenditure for James Bay and Sal de Vida remain subject to the same cost pressures that all resource projects are experiencing globally. Allkem will continue to review and monitor the capital cost budgets for all its projects as they progress.”

Financials and Corporate

- “Group revenue for the quarter was $298 million and group gross operating cash margin1 was 82%, approximately US$244 million.

- At 30 September group net cash5,6 was US$447 million up US$28.9 million from 30 June 2022. This figure excludes US$52.1 million of cash receivable related to Mt Cattlin’s September shipments that has been received in October.

- Allkem entered into a binding and conditional Heads of Agreement (“HOA”) to acquire 100% of the strategic lithium tenement of María Victoria located in the Olaroz basin and to divest its investment in Borax Argentina S.A (“Borax”).

- Post reporting period, Allkem and the International Finance Corporation (“IFC”) agreed to a non-binding term sheet for a US$200 million project financing facility for the Sal de Vida Project, subject to final commercial terms to be agreed and IFC and Allkem board approvals.

- The business is entering a period of significant growth with Naraha to begin commercial production later this year, Olaroz Stage 2 first production in the first half of next year, Sal de Vida scheduled to commence production in late 2023 and James Bay in mid-2024.”

Upcoming catalysts include:

- Late 2022 – Naraha to begin commercial production.

- H1, 2022 – Olaroz Stage 2 expansion commissioning followed by a 2 year ramp to 25ktpa. When combined with Stage 1 total capacity will be 42.5ktpa.

- Late 2023 – Sal De Vida Stage 1 production targeted to begin and ramp to 15ktpa. SDV Stage 2&3 combined will begin about 2025 and ramp to an additional 30ktpa. Total combined when completed will be 45ktpa.

- Mid 2024 – James Bay production targeted to start.

You can read the latest investor presentation here. You can read the latest Trend Investing Allkem article here.

AMG Advanced Metallurgical Group NV [NA:AMG] [GR:ADG] (OTCPK:AMVMF)

No news for the month.

Upcoming catalysts:

- Q4, 2022 – Lithium-vanadium battery (“LIVA”) for the energy storage market to be ready.

- End Q4, 2022 – New vanadium spent catalyst recycling facility in Zanesville, Ohio to be commissioned.

- Q2, 2023 – Stage 2 production at Mibra Lithium-Tantalum mine (additional 40ktpa) forecast to begin, bringing total production capacity to 130ktpa.

- Q3, 2023 – Lithium hydroxide facility in Bitterfeld-Wolfen Germany to be commissioned. First module to be 20,000tpa LiOH.

- 2023 –> Saudi Arabia vanadium Projects JV with Shell & Aramco.

- 2025-2028 – German LiOH facility expansion with Modules 2-5 (100,00tpa LiOH.

You can view the latest company presentation here or the very recent Trend Investing article here.

Lithium Americas [TSX:LAC] (LAC)

On October 7, Lithium Americas announced:

Lithium Americas confirms oral hearing schedule for the Thacker Pass record of decision appeal. “With all state and federal permits received to begin construction, the ruling on Thacker Pass’ ROD represents the final regulatory hurdle to move forward the largest and most advanced lithium chemicals project in the US,” said Jonathan Evans, President and CEO. “We stand ready to develop a critical source of lithium supply, creating jobs and enabling a more sustainable battery ecosystem in North America. As we await a ruling by the Federal Court, we are moving ahead with all areas required to support construction, including final selection of an EPCM contractor, evaluating partnership and supply agreements, as well as progressing our application with the US Department of Energy loan program.”

On October 20, Lithium Americas announced: “Lithium Americas signs community benefits agreement with Fort McDermitt Paiute and Shoshone Tribe.”

Upcoming catalysts:

- H2 2022 – Thacker Pass FS and early construction works planned to commence.

- H2 2022 – Cauchari-Olaroz lithium production to commence and ramp to 40ktpa. From 2025 a Stage 2 20ktpa+ expansion is planned.

- 2023 – Possible lithium clay producer from Thacker Pass Nevada (full ramp by 2026).

NB: Ganfeng Lithium (51%) and Lithium Americas (49%) own the JV company Minera Exar S.A., which owns 91.5% interest and is entitled to 100% of the production from the Cauchari-Olaroz Project. The 8.5% interest is owned by Jujuy Energia y Mineria Sociedad del Estado (“JEMSE”) (a company owned by the Government of Jujuy province).

Argosy Minerals [ASX:AGY][GR:AM1] (OTCPK:ARYMF)

Argosy has an interest in the Rincon Lithium Project in Argentina, targeting a fast-track development strategy. Argosy is now producing at a small scale and ramping to 2,000tpa lithium carbonate starting June 2022.

On September 23, Argosy Minerals announced: “Resource expansion & production well drilling progressing at Rincon.”

On October 3, Argosy Minerals announced: “Rincon 2,000tpa Li2CO3 operational update.” Highlights include:

- “97% of total development works complete – with plant commissioning 81% complete.

- Current commissioning works successfully producing primary lithium product.

- Steady-state lithium carbonate production operations scheduled during next quarter.”

Upcoming catalysts:

- Oct. 2022 – Rincon Lithium Project commissioning.

Investors can view the company’s latest investor presentation here, and the latest Trend Investing Argosy Minerals article here.

Core Lithium Ltd. [ASX:CXO] [GR:7CX] (OTC:CORX)(OTCPK:CXOXF)

Core 100% own the Finniss Lithium Project (Grants Resource) in Northern Territory Australia. Significantly they already have an off-take partner with China’s Yahua (large market cap, large lithium producer), who has signed a supply deal with Tesla (TSLA). The Company states they have a “high potential for additional resources from 500km2 covering 100s of pegmatites.” Fully funded and starting mining with a planned Q4 2022 production start.

On September 29, Core Lithium announced: “Business update: Finniss DSO shipment preparations, and BP33 diamond drilling results.” Highlights include:

Finniss operations

- “Uncovered first spodumene ore at Finniss in September.

- First lithium, Direct Ship Ore (DSO) shipment preparations are underway.”

BP33 exploration

- “High grade spodumene bearing pegmatite intersected in multiple holes at BP33, up to 830m below surface.

- New spodumene intersections more than 400m outside of the current Mineral Resource at BP33 expected to deliver substantial orebody extensions.

- High-grade lithium intersections, including: 22.85m @ 1.59% Li2O in NMRD032. 15.31m @ 1.62% Li2O in NMRD034.”

On October 3, Core Lithium announced: “Successful completion of A$100m placement to accelerate growth initiatives at Finniss.” Highlights include:

- “…Significantly strengthened balance sheet will enable Core to fast-track exploration programs, expedite capital development initiatives and pursue further organic and inorganic growth opportunities.”

On October 5, Core Lithium announced: “BP33 diamond drilling assays.” Highlights include:

- “High-grade spodumene bearing pegmatite confirmed in multiple holes at BP33, up to 830m below surface.

- High-grade lithium intersections, including: 72.74m @ 1.56% Li2O in NMRD038. 22.0m @ 1.60% Li2O in NMRD039.

- New spodumene intersections more than 400m outside of the current Mineral Resource at BP33 expected to deliver substantial extensions.

- Accelerated Resource definition and extension drilling planned at BP33 and across the Finniss Project more broadly.

- Recent funding also enables Core to bring forward development and early works at the proposed BP33 mine.”

On October 10, Core Lithium announced: “Primero awarded operations and maintenance contract for Finniss Lithium DMS Plant.” Highlights include:

- “…Project execution to start immediately for an initial term of five years.

- Commissioning of the DMS plant and first production of lithium concentrate scheduled for H1 2023.”

Investors can read a company presentation here, or the Trend Investing article when Core Lithium was back at A$0.055 here.

Catalysts include:

- H1 2023 – Lithium spodumene concentrate production at Finniss targeted to begin.

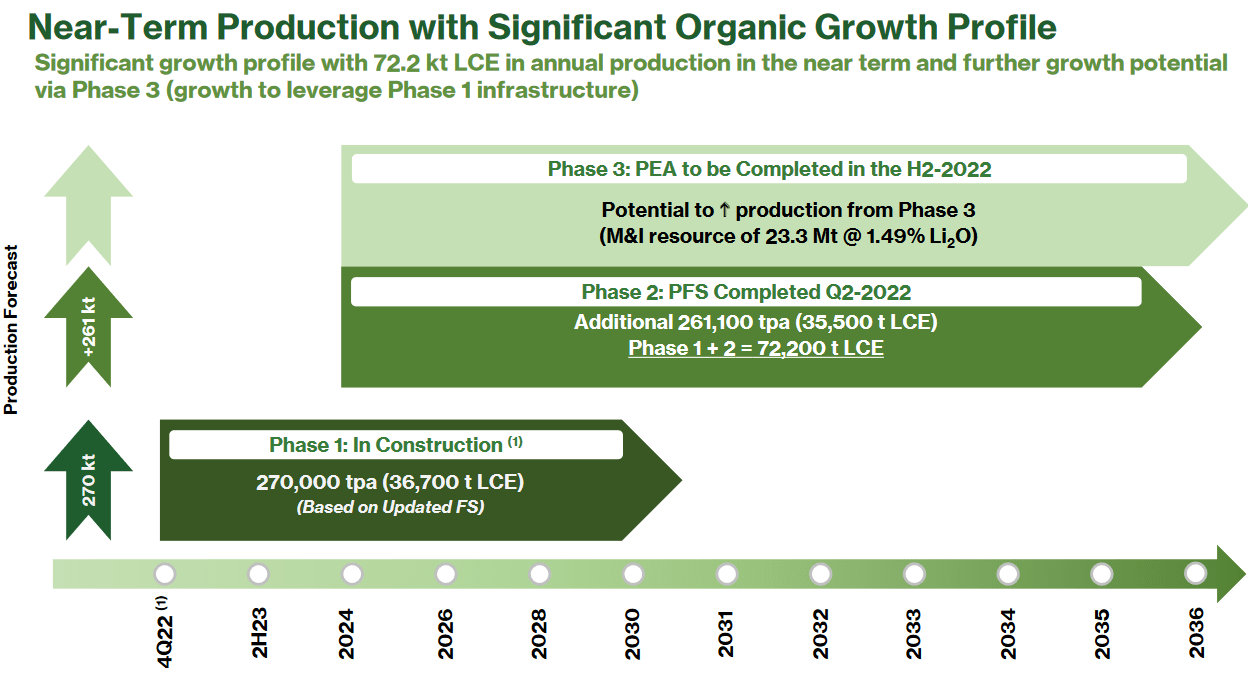

Sigma Lithium Resources [TSXV:SGML] (SGMLF) (SGML)

Sigma is developing a world class lithium hard rock deposit with exceptional mineralogy at its Grota do Cirilo Project in Brazil.

No news for the month.

Catalysts include:

- Late 2022 – Commissioning at the Grota do Cirilo Project.

- H1 2023 – Commercial production targeted to begin at the Grota do Cirilo Project in Brazil and ramp to 531,000tpa spodumene (Stage 1 and 2 combined).

Investors can read the latest company presentation here or the Trend Investing article here back when Sigma was trading at C$5.00.

Sigma Lithium has very large production plans

Sigma Lithium company presentation

Lithium miner ETFs

The LIT fund was slightly down in October. The current PE is 17.34.

Our model forecast is for lithium demand to increase 5.3x between end 2020 and end 2025 to ~1.8m tpa, and 13x this decade to reach ~4.5 m tpa by end 2029 (assumes electric car market share of 32% by end 2025 and 70% by end 2029).

Note: A Nov. 2020 UBS forecast is for “lithium demand to lift 11-fold from ~400kt in 2021 through to 2030.”

Global X Lithium & Battery Tech ETF (LIT) 10 year price chart

Seeking Alpha

- The Amplify Lithium & Battery Technology ETF (BATT) is currently on a PE of 11.12. It is a well diversified fund. On their website they state: “BATT is a portfolio of companies generating significant revenue from the development, production and use of lithium battery technology, including: 1) battery storage solutions, 2) battery metals & materials, and 3) electric vehicles. BATT seeks investment results that correspond generally to the EQM Lithium & Battery Technology Index (BATTIDX).

Conclusion

October saw new record highs for lithium prices as demand continues to outrun supply.

Highlights for the month were:

- Rio Tinto warns planned lithium production will fail to meet growth in demand for lithium-ion batteries.

- CATL plans $1.9 billion battery project in China’s Luoyang City.

- NASA solid-state battery is lighter & more powerful.

- Morgan Stanley: We expect the market to remain tight through 2022, especially when considering restocking needs.” “We still expect lithium prices to trend lower in 2023, as supply expands and market tightness eases…”

- BMI: Lithium has to scale twenty times by 2050 (from 2021 levels) as automakers face generational challenge.

- Elon Musk stated: “We continue to believe that battery supply chain constraints will be the main limiting factor to EV market growth in the medium and long terms.”

- Biden-Harris administration awards $2.8 Billion of grants to supercharge U.S. manufacturing of batteries for electric vehicles and electric grid… The American Battery Material Initiative will coordinate domestic and international efforts to accelerate permitting for critical minerals projects.

- Albemarle secures ~$150M DoE grant for U.S.-based lithium facility at Kings Mountain, North Carolina.

- Ganfeng will invest another RMB 30 billion in Yichun, Asia’s lithium capital. Ganfeng Lithium’s Q1-Q3 2022 net profit projected to soar 478.29%-518.73% YoY.

- Tianqi Lithium positive profit alert (up 2,768.96% to 3,089.83%).

- Pilbara Minerals achieves two record BMX spot auction spodumene (5,000t each) sales in October at equivalent of ~US$7,830/dmt and US$8,000/dmt.

- Mineral Resources believes it can build a 50,000tpa LiOH plant in WA for US$650m. MinRes is targeting 120,000tpa LCE production from the Wodgina and Mt Marion mines in the next five years. JPMorgan assessing potential spin-off structures, and a potential US listing for the MinRes lithium business.

- Allkem receives US$200m IFC project finance facility proposal for Sal de Vida. Allkem divests its investment in Borax Argentina S.A. Allkem’s business is entering a period of significant growth.

- Lithium Americas confirms oral hearing schedule for the Thacker Pass record of decision appeal.

- Argosy Rincon Project 97% of total development works complete, plant commissioning 81% complete.

- Core Lithium prepares to start DSO operation. Commissioning of the DMS plant and first production of lithium concentrate scheduled for H1 2023.

As usual all comments are welcome.

Source: news.google.com

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}