Michael M. Santiago/Getty Images News

The sudden collapse of SVB Financial Group (SIVB) and a few other banks has pressured the stock of Wells Fargo & Company (NYSE:WFC). The issue is mostly a crisis of confidence when the large banks have massive amounts of insured deposits escaping the uninsured deposit risk of the closed banks. My investment thesis is ultra Bullish on WFC stock, especially after this massive dip back to $40.

Source: Finviz

Deposit Costs

While Wells Fargo doesn’t face a liquidity crisis similar to SVB, the large financial does have issues with deposit costs. The company discussed at the 24th Annual Financial Services Forum that deposits were generally trending down along the lines of expectations, with consumers spending some of their balances and investment funds moving towards more attractive rates.

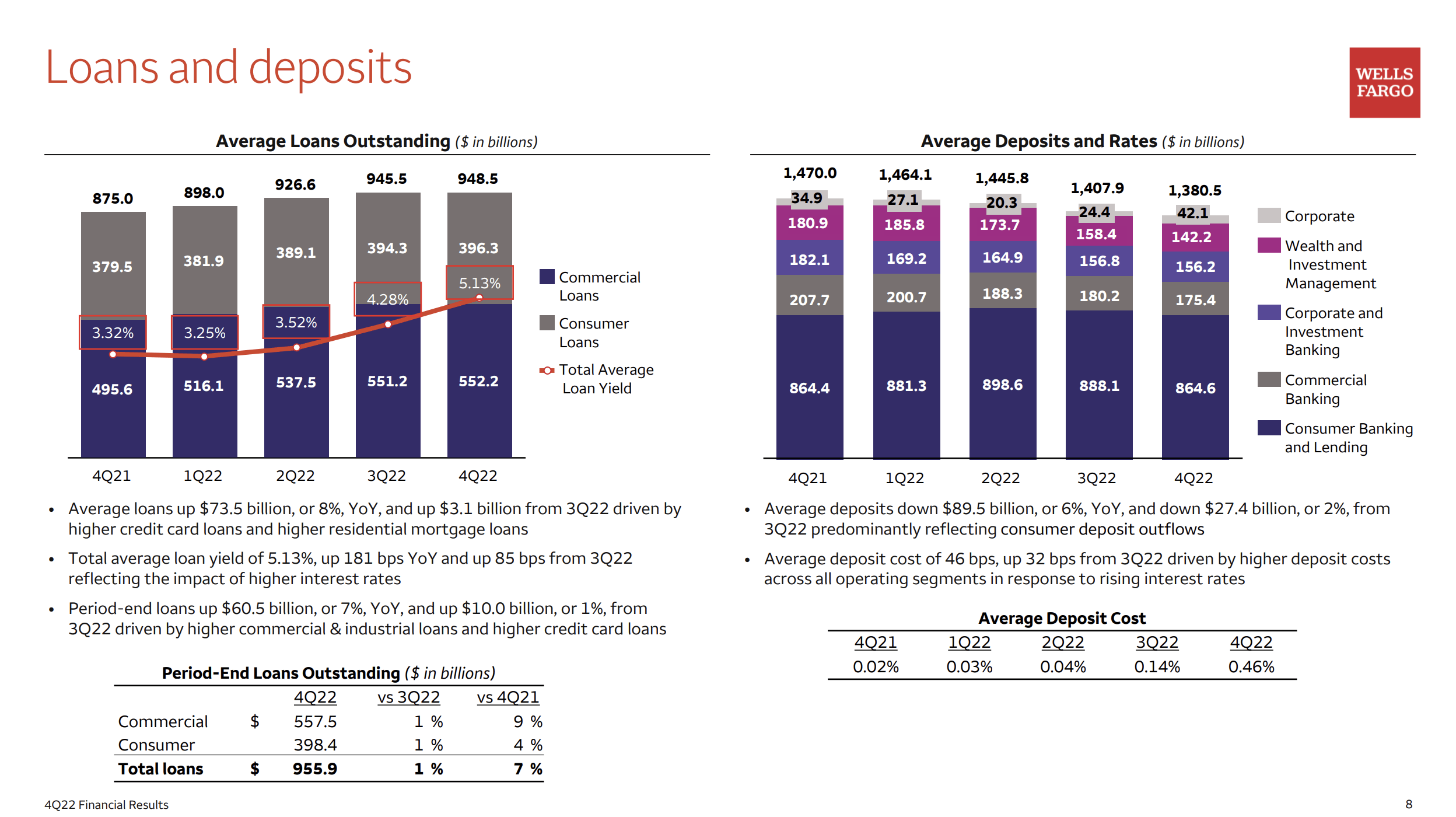

Wells Fargo ended 2022 with a deposit balance of $1.38 trillion. The large bank only has an average loan balance of $949 million, with limited capacity to expand the business anyway due to the asset cap.

Source: Wells Fargo Q4’22 presentation

Back during Q4’22, Wells Fargo saw the average deposit cost jump 32 basis points to 0.46%. The banking sector entered this crisis facing a general problem of now having to pay for deposits after years of virtually no costs.

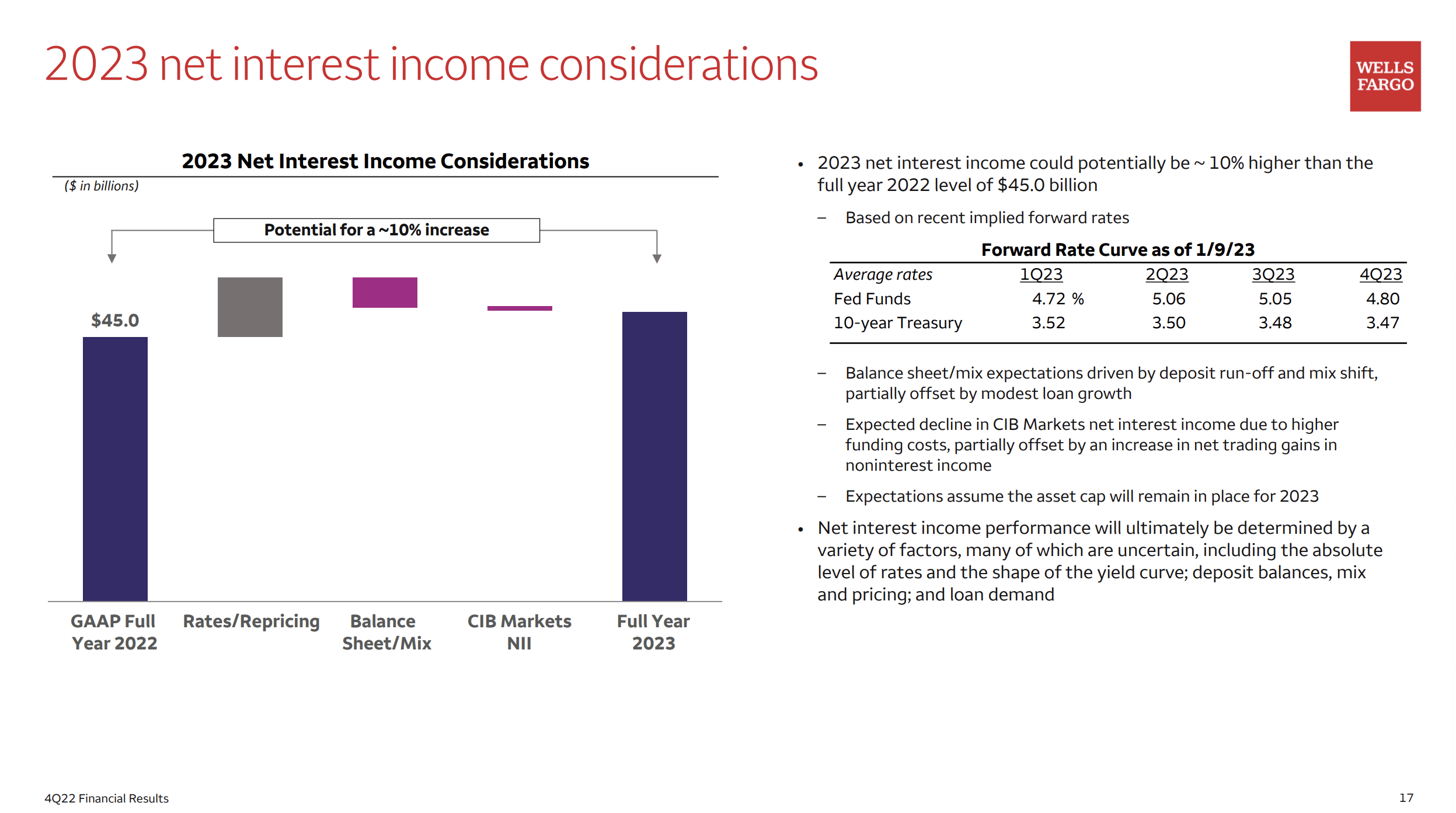

Even with the deposit issue, Wells Fargo predicted a nearly 10% boost in NII in 2023 to ~$50 billion. The large bank earned $13.4 billion in NII during Q4, so the forecast would in essence be for a reduction in the quarterly NII to only $12.5 billion.

Source: Wells Fargo Q4’22 presentation

The quarterly NII would be far above the prior period levels outside Q4. The key, though, is that Wells Fargo has a large focus on retail deposits from branch banks limiting the withdrawals and the ultimate costs.

Per calculations from Reuters, the bank has less than 50% of deposits from uninsured balances. Wells Fargo has far lower uninsured balances at risk of flight unlike SVB and other smaller regional banks facing pressure over the last week.

If anything, Wells Fargo is likely to have seen some deposits flee SVB and other regional banks for the relative safety of the larger bank. The deposit base could be higher at the end of Q3.

HTM Portfolio Not A Problem

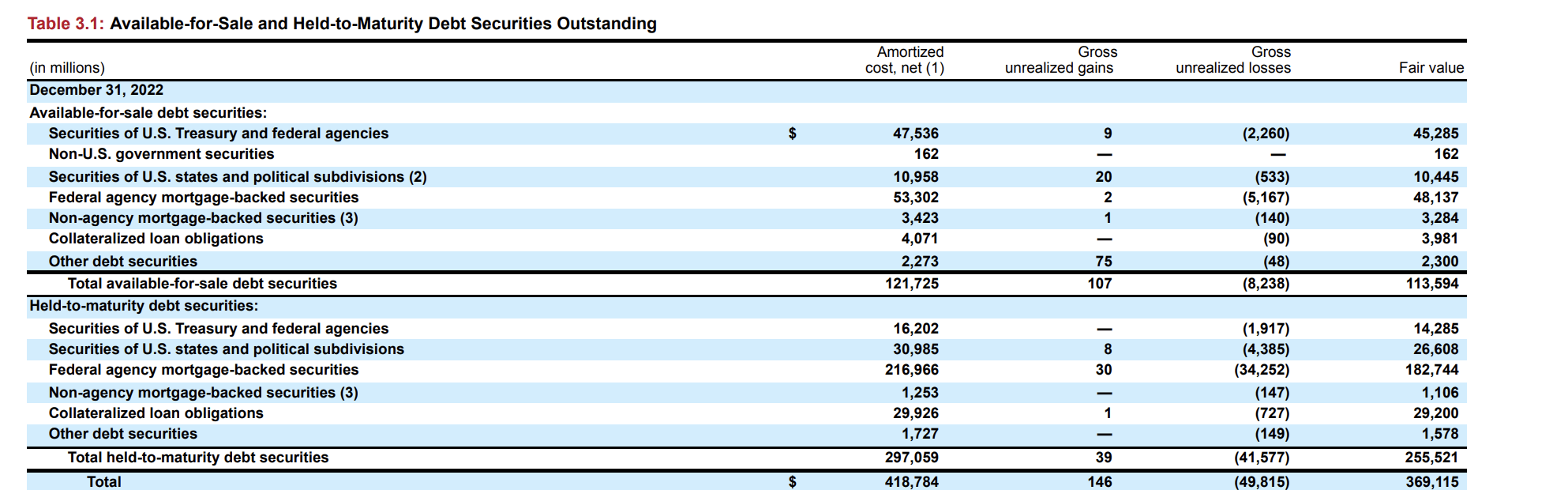

At the end of 2022, Wells Fargo held $294 billion worth of HTM (Held-to-maturity) securities compared to $103 billion for AFS (Available-for-sale). In addition, the large bank had a cash balance of $127 billion providing plenty of liquidity in the cash balance and the AFS portfolio to handle any deposits fleeing.

Wells Fargo had ~$42 billion in unrealized losses in the HTM portfolio. Since these securities are being held-to-maturity, the large bank won’t incur any actual losses on this bond portfolio unless the company is forced to sell these securities prior to maturity.

Source: Wells Fargo ’22 10-K

The suddenly lower bond rates will help these unrealized loss totals shrink when reporting results for the end of March. Regardless, Wells Fargo would have to burn through other assets before the HTM portfolio comes into play, while these bonds are constantly being burned down and repriced at higher rates.

The large bank had a balance of $133.5 billion in capital now, so even a complete repricing of the HTM portfolio wouldn’t burn through the capital at Wells Fargo. Now, the large bank would have issues with capital ratios and capital would need to be raised, but Wells Fargo is in no position where the company faces such an outcome.

SVB had unrealized losses on HTM securities that matched their capital position. The bank faced issues with panicked uninsured depositors fleeing the bank with some analysts now suggesting depositors from SVB and Signature Bank (SBNY) have boosted the deposits of other banks.

Prior to this crisis, Wells Fargo was on the path to earning $5+ per share by at least 2024. At $40, the stock is an extreme bargain whether or not the current crisis disrupts the earnings stream, though that doesn’t appear the base case yet.

Takeaway

The key investor takeaway is that the selloff in Wells Fargo is irrational. The large bank has probably acquired deposits during this crisis. Wells Fargo & Company stock is cheap, trading at only 7x 2024 EPS targets.

Source: seekingalpha.com

{kind=link}

{kind=link}

{kind=link}