NicoElNino/iStock via Getty Images

Introduction

PNC Financial (NYSE:PNC) reported earnings this morning and the headlines read “PNC Financial GAAP EPS of $3.98 beats by $0.34…” The immediate reaction after the market opened sent the stock price down roughly -1%, and as I’m proofreading this article, it’s down -2.5%. I’m sure there are many investors who may be scratching their heads at the disconnect. And while it’s true that immediate market moves post earnings can reflect a variety of factors (and the stock price might move higher before I finish writing this article) this is a case where an “earnings beat” isn’t really an earnings beat. In this article, I will explain why this is so. I’ll also share three things I think potential PNC stock owners should consider before buying. But, before we get into that, I will share my history with this stock to hopefully establish a little credibility since I’m offering up what will be a contrarian view for many.

My History With PNC Stock

I first warned investors about PNC’s deep historical price cyclicality all the way back on May 9, 2018, in my article “How Far Could PNC Financial Fall?” My approach at the time was less refined than it is now, but my warning to investors was clear.

PNC has consistently fallen 40%-70% during recessions and it has usually been a good leading indicator of market trouble a couple years in advance of major market decline. Was January the peak? I don’t know for sure. But I think it seems like a reasonable time to get more defensive with a less cyclical allocation with the hopes of buying PNC stock closer to the bottom of the cycle.

As it turned out, I did end up eventually buying PNC closer to the bottom of the cycle. I first purchased PNC stock in my investing group, The Cyclical Investor’s Club, during the March 2020 crash, and it just so happened I bought on the same day the market bottomed 3/23/20. Here’s how PNC performed from the publication of my warning article until I purchased the stock a couple of years later:

My caution in 2018 was justified, and even before the big March crash (which I certainly didn’t know was coming in 2018), PNC already had underperformed the S&P 500 by a wide margin.

My eventual purchase wasn’t based on a macro call so I had no idea the day I bought PNC would be the bottom in the wider market. My purchase was based on individual metrics for PNC stock. I wrote a public article about the PNC purchase a couple months later as part of a 20-article series on all the S&P 500 stocks I bought during the March 2020 crash. It was titled “Stocks I Bought On The Dip: PNC Financial.” In that article, I explained the entire process I used in deciding when to buy PNC stock. Importantly, this process had been refined quite a bit from my original coverage of PNC stock back in 2018. The key change in my process had to do with differences in price cyclicality and earnings cyclicality. Before 2019, I focused only on stock price cyclicality, but starting around 2019, I realized that there were some stocks that had much deeper price cyclicality than they had earnings cyclicality. This was important because around that time I used different strategic approaches based on earnings cyclicality, and PNC actually only had moderately-deep earnings cyclicality historically, while price cyclicality was much deeper.

This realization of the misalignment of price vs. earnings basically created a new category of stocks for me, and it allowed me to safely aim for lower purchase prices during downturns for stocks of this type. It also caused me to get more cautious near the potential tops of business cycles and allowed me to take profits sooner than I otherwise might have. Based on this, I decided to sell almost all stocks that fit this category in January 2022, and I wrote about them in my article “6 Financial Stocks I Recently Sold And 2 I will Hold For The Long Term.” One of those financial stocks I sold was PNC. Here’s how I ended up doing with that investment:

I did extremely well on my PNC position. (And before anyone thinks I’m bragging or cherry-picking, if you read my linked article above, you’ll see one of the financial stocks I decided to hold onto – and the only one I still held going into this year – was Signature Bank, and it went to zero. So even I’m not perfect.) Since I sold PNC, here is how it has performed:

What I’m trying to show here is that when I write bearish articles I don’t have some axe to grind, and when I aim for low buy prices they do have a reasonable chance of actually hitting. And when they do hit, they stand to make a lot of money.

With that background, here are what I think investors should think about right now.

This Wasn’t Really An Earnings Beat By PNC Financial

The headline after this quarter’s earnings was that PNC beat by $0.34. Another news outlet had them beating estimates by about $0.32, so the general consensus was pretty close in terms of quarterly expectations. For this year, Seeking Alpha’s consensus was $14.42 per share.

Seeking Alpha

The estimate on FAST Graphs, which I’ll highlight in a moment, was $14.60 per share (so a little more optimistic and in line with ‘beat’ we just saw reported).

Sometimes, during times like this, it’s useful to zoom out and understand a few basic investing dynamics for context. Investors who are purchasing stocks based on fundamentals like earnings (which is what I have done historically when buying PNC) must take a longer-term view than traders who are just trading short-term sentiment. The reason for this is that the correlation between the stock price and earnings isn’t very strong over short periods of time, but it increases over longer periods of time so that if we could predict earnings 20 years from now, we could fairly accurately predict the stock price within some reasonable range. Because of this dynamic, predicting earnings a week into the future right before they are reported for a quarter isn’t very useful for the investors who actually use earnings to value stocks. What’s more important are what earnings are expected to be one year or two years out because it provides a better trajectory of where longer-term earnings might be going.

FAST Graphs

Because I have been publishing regularly on PNC I’ve actually logged what analysts were expecting in terms of 2023 and 2024 earnings in the past. If we take the more optimistic FAST Graphs expectation of $14.60 and add on the $0.34 of earnings “beat” this quarter we’re up to $14.94 for 2023. This is far, far, below the $16.57 analysts were expecting just six months ago. So, I hardly consider this an earnings beat. Analysts expected far more earnings six months ago than they’re getting right now. Additionally, we will have had around 15% cumulative inflation from 2021-23 when it’s said and done, so these misses are even worse in terms of purchasing power.

My main message here is not to let quarterly headlines mislead you from the bigger, more meaningful, picture that’s taking place regarding earnings. Stay focused on the actual numbers rather than how wrong analysts have been.

Recession P/E Factor

I’ve written several articles recently that explain my overall process for valuing a stock that has moderately cyclical earnings, yet deep price cyclicality. These types of stocks (as I have shown) can give investors tremendous opportunities for above average returns, but the best returns require making an approximate recession call. The call does not have to be precise. If it’s within 2-3 years, that’s usually close enough. I sold PNC in January of 2022 and we haven’t had a recession, yet. But an investor does need to understand when recession risk is high, so that they don’t buy the stock too soon (before the recession). By definition, these stocks have deep price cyclicality. I believe that recession risk is very high right now. However, if you believe 1) recession risk is not high, or 2) we’re already in a recession, then PNC’s buy price is about $145.35 and below that it looks good based on $14.60 earnings expectations for this year. I’m not in this camp, however, because I do not think we’re currently in a recession, but are likely to be in one in the near future, so the worst is likely yet to come. For that reason, I’m not a buyer, yet. (If you’re interested in the process I went through arrive at that buy price, read my last PNC article or two where I explain the entire valuation process.)

The factor I like to pay attention to with a deep price cycle stock that only has moderately cyclical earnings is what I call the “Recession P/E.” The simplest explanation of this is to look back at what P/E the stock traded at in previous recessions, and on a monthly basis, according to FAST Graphs, I see a 6.65 P/E for the 2020 drawdown, and that’s what I’m currently using as my guide for when to buy PNC stock. (If a person wanted to be more conservative, the recession P/E for 2008 was 4.87. And if the financial system experiences a similar collapse this time around, I would consider adjusting my recession P/E down to that level, but, so far, that is not my expectation.)

If we use the current $14.60 expectation for this year this implies a buy price around $97.09, and if we assume this expectation goes up $0.34 after earnings (which, I’m not sure it will) then based on $14.94 in earnings this year the buy price would be $99.35. So, basically, right now, I don’t think PNC stock is a buy until it falls at least below $100 per share, and the buy price might become even lower if earnings expectations decline more as time goes on this year. Additionally, if we do see a real banking crisis, we might need refer to 2008’s recession P/E instead of 2020’s. I’ll write an update article if that should happen.

Recovery Time

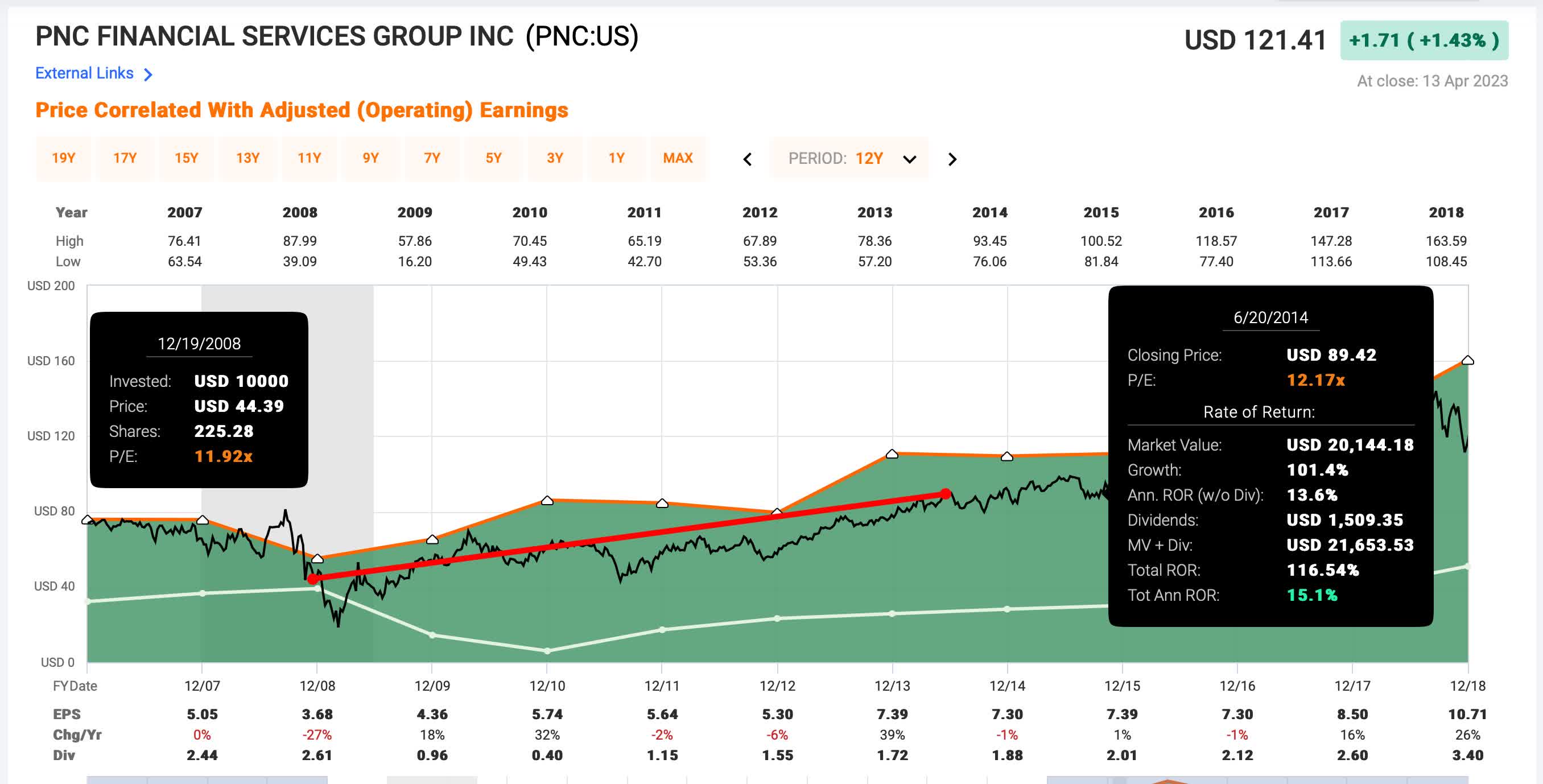

The third consideration investors need to think about is the length of time it might take for the stock price to reach a new cyclical peak. The 2020 cycle was dramatically compressed and should not be expected to repeat in such a short period of time. Additionally, if interest rates normalize at a higher level than they did post 2008, it could be an additional drag on general economic performance. And while normalization would likely be good over the long-term for banks, the medium-term could be tougher than investors expect.

As I write this, PNC stock is about -48% off its highs. If a person would have bought around these levels in late 2008, it would have taken about six years (instead of less than two years from 2020-22) for the stock price to make new highs again.

FAST Graphs

Buying PNC at that point would have produced pretty good absolute returns over these 6.5 years with a +116% total return. But that actually would have underperformed the S&P 500 over this same time period.

Because I aim to get better returns than the wider market, I really want to be buying at a price where my returns are superior, and if we have a longer, more drawn-out recovery as we did in post 2008, then I need to buy PNC stock lower than it trades right now if history roughly repeats.

Conclusion

My goal of this article was mostly to present some different angles from which to look at this stock and to share how I actually think about it. I’m well aware they aren’t the typical ways the standard analyst is going to look at it. But the stock market is a place that usually requires unique ways of looking and acting in order to get superior returns. Right now, I think it’s wise for investors seeking above-average medium-term and long-term returns to wait for a better price.

Source: seekingalpha.com

{kind=link}

{kind=link}

{kind=link}