Goldman Sachs Tower – Exchange Place, Jersey City NJ

BackyardProduction

Summary

Years ago, while growing up on the New York City waterfront, I remember looking up at the construction of the new Goldman Sachs Group (NYSE:GS) tower on the Hudson waterfront in downtown Jersey City, an area known as “Wall Street West” due to the influx of financial firms from across the river in NYC.

This firm, with NYC roots that go back to 1869, has weathered two centuries of turbulent market waves.. much like the waves from New York harbor crashing against the walkway beneath the giant tower, whenever a storm wails through.

Today, as an analyst on Seeking Alpha, despite recent banking sector headwinds and storms I am giving Goldman Sachs stock a Buy rating, and here is why…

When rating bank stocks, I have put together a very straightforward 4-part methodology that answers the following four questions and tells a story for an investor:

- Does the stock pay a competitive dividend yield with dividend growth?

- Is this bank in a healthy capital position based on CET1 ratios?

- Does it have diversification in its business segments or is it too exposed to one banking segment such as consumer banking?

- Does the current price chart indicate a bearish trend and buying opportunity, using the “golden cross / death cross” method?

When it comes to Goldman Sachs, my analysis has concluded that it is offering a competitive dividend yield with proven dividend growth, it is in a strong capital position, it has diversified business segments and is not exposed completely to consumer banking, and the current price chart indicates a buying opportunity for a long-term investor.

Although my methodology is not the only one you can use, below I will demonstrate why it tells me the “story” I need to make a quick and informed trading decision from just a few key data points that I believe to be relevant, ignoring a lot of other background noise.

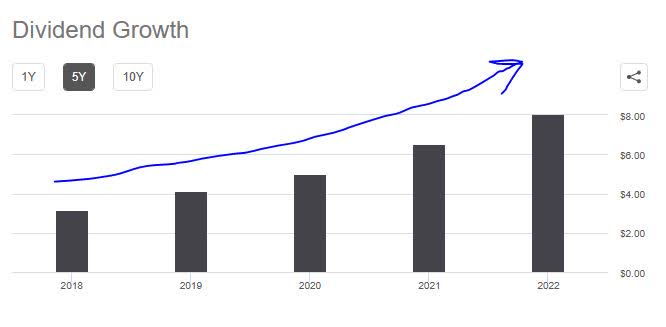

Their dividend yield is attractive, with proven 5 year dividend growth

This stock pays a dividend of $2.50 per share, with a yield of 3.07%, according to dividend info on Seeking Alpha.

In addition, when looking at the chart below, the stock has had dividend growth over the last 5 years. Though future dividends are not guaranteed, I could extrapolate this graph over the next five years using the same YoY growth percentages, to get a calculated guess at potential future dividends.

……………………………………………………………………………………………..

Goldman Sachs – 5 year dividend growth (Seeking Alpha)

……………………………………………………………………………………………..

The reason I like dividend stocks is twofold: it tells me a company is in a healthy enough cash position that it can return capital back to shareholders, and for shareholders it provides a recurring source of quarterly income just from holding the stock. In fact, the longer you hold it the more dividends you will earn.

My viewpoint was shared by a February 2023 article in Seeking Alpha by Nick Ackerman and Cash Builder Opportunities. The article had the following points to share:

For investors, dividends can provide a steady stream of income and can also be a sign of a company’s financial health. They are most often associated with being held by retirees, but that doesn’t always have to be the case. Simply put, dividend investments can really be for any investor.

It also is a passive way to generate income, for the most part.

The next question is whether this stock’s dividend is competitive in relation to some of its banking sector peers. Let’s take a look:

The dividend yield of Morgan Stanley (MS) is just slightly higher at 3.77%, Charles Schwab (SCHW) has a current yield of 1.94%, and America’s top bank JPMorgan Chase (JPM) currently has a yield of 2.87%.

Hence, the evidence shows that Goldman is definitely competitive within its sector when it comes to dividend yield.

Why focus on the yield? Because it gives me an idea of the return I am getting on the capital invested, since you can score a higher yield in cases where the share price goes down, since you are getting more shares for the same capital, and you can earn more dividend income then on that same capital.

My approach to comparing dividend yields in the same sector was echoed by a February article in Forbes:

When evaluating dividend yields, it’s important to compare the yields offered by companies in the same industry—or funds in the same category—since yields can vary greatly across sectors, industries and fund categories.

In other words, I would not be comparing Goldman side by side with Microsoft (MSFT) or Amazon (AMZN), but with companies in the same sector, and further then with banks in the bulge bracket.

They have a healthy capital position as a systemically critical bank

As one of the global systemically critical banks listed by the Financial Stability Board, I think Goldman Sachs will continue to have analysts’ eyes and ears on its capital situation constantly, and based on its first quarter capital ratios below it is in no trouble anytime soon in this category alone.

……………………………………………………………………………….

Goldman Sachs – Q1 2023 – CET1 Capital Ratios (Goldman Sachs)

……………………………………………………………………………….

Some of you may already know that based on the Basel 3 requirements, the minimum CET1 should be 4.5%. From the Wikipedia article on this topic as well, the banks are expected to maintain a leverage ratio in excess of 3% under Basel III.

Goldman Sachs currently is well above those levels as we can see.

By comparison, a much smaller regional banking group like Regions Financial (RF) had a CET1 ratio in that same quarter of 9.8%, according to their own quarterly earnings release.

I would be hesitant to buy shares in a bank with very low CET1 ratios, because banks need to be able to adequately absorb shocks to the system so they don’t become insolvent, especially since bank insolvency has shown recently to create a ripple effect in both its sector and overall markets.

My view is supported by an April 2022 article in Investopedia on the topic of CET1 ratios:

A low CET1 ratio implies an insufficient level of Tier 1 capital. In such a case, a bank may not be able to absorb a financial shock and may need to be bailed out quickly in the event of a financial crisis.

Rather than being in danger of being bailed out, Goldman Sachs actually was one of the banks that initially came to the rescue of struggling First Republic Bank (OTCPK:FRCB) this spring with a massive deposit infusion.

As the March 16 article in the Guardian mentioned, “Goldman Sachs and Morgan Stanley are each making deposits of $2.5 billion.”

The firm has a diversified basket of income streams not limited to consumer banking

From the firm’s website, The firm is diversified among three business segments: asset and wealth management, global banking and markets, and platform solutions. In addition, it has an in-house research shop as well, called its global investment research division.

First, let’s see how its different segments did in the first quarter.

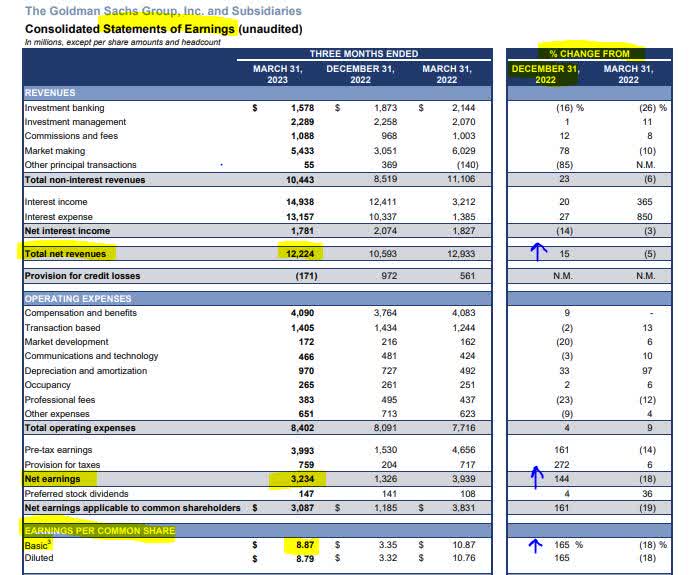

The following are taken from the Goldman Sachs Q1 2023 earnings results.

…………………………………………………………………………………………….

Goldman Sachs – Q1 2023 – Consolidated Earnings (Goldman Sachs)

…………………………………………………………………………………………….

While net revenues, net earnings, and earnings per share increased vs the prior quarter ending Dec. 2022, more important to my thesis is that its revenues came from multiple streams, three of which performed better than in the prior quarter, offsetting the ones that did not.

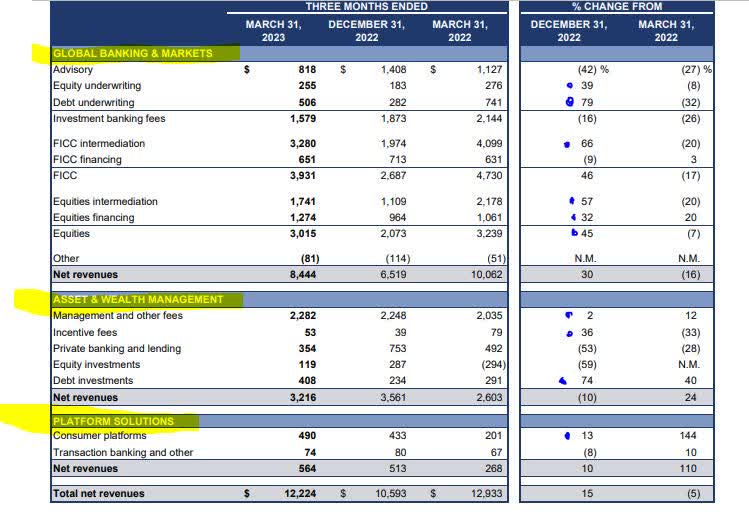

Here is another look at how the firm is distributed among its key business segments:

……………………………………………………………………………………………..

Goldman Sachs – Q1 2023 – Results by Segment (Goldman Sachs)

……………………………………………………………………………………………..

For example, within its division of global banking and markets, its revenue from equities underwriting alone was $255MM in the first quarter, a 39% increase vs the prior quarter. And, while its advisory business seemed to take a drop vs the prior quarter, it still brought in $818MM in revenue in the first quarter of this year.

I also want to highlight that this firm is a major market maker, and you can see from the table above that this is another money-making source for them, but I would say is also a critical component to the larger trading ecosystem.

In its brief lesson on what market makers do, Corporate Finance Institute also reiterated my view of their systemic importance in a March 2023 article on market making:

The purpose of market makers in a financial market is to keep up the functionality of the market by infusing liquidity. They do so by ensuring that the volume of trades is large enough such that trades can be executed in a seamless fashion.

In the absence of market makers, an investor who wants to sell their securities will not be able to unwind their positions. It is because the market doesn’t always have readily available buyers.

On the flip side, it is important that I mention their experiment in consumer banking called “Marcus”, which has proven to be a loss-making endeavor, and is also one of their business segments along with the others.

I want to continue to monitor the next few quarters to see what they do with this concept.

An April 2023 article in the New York Post highlighted the headwinds they faced in consumer banking:

‘The events of the first quarter acted as another real-life stress test, demonstrating the resilience of Goldman Sachs and the nation’s largest financial institutions,’ Goldman Sachs CEO David Solomon said in a statement.

In February, Solomon said Goldman was exploring strategic alternatives for Marcus, which has lost more than $3 billion since its debut in 2020. The bank is attempting to stabilize its business amidst an internal shift that included thousands of layoffs.

However, the evidence my investing thesis presents clearly shows that this firm was able to offset the losses in that segment with its many other more successful segments.

In my opinion, that is an example of a well-diversified business model that can withstand shocks and stress. In addition, Goldman is not traditionally a consumer bank but an investment bank.

What we saw with the early spring bank failures of Silicon Valley Bank (SVB) and Signature Bank (OTC:SBNY) was a problem of liquidity, which Goldman Sachs does not have a problem with.

In the case of those regional banks, the US Government Accountability Office summed up the issue well in an April article:

Funding rapid growth with uninsured deposits—deposits that exceed the $250,000 FDIC insurance limit—increased risks to the banks. Customers with uninsured deposits may be more likely to withdraw their funds, or “run” on the bank, during times of economic uncertainty.

The stock’s current chart indicates a bearish trend, which is a buying opportunity

The price chart below shows this stock’s price from December 2022 until May 19 2023, with an overlay of the 50 day simple moving average (dark blue line) and the 200 day simple moving average (dark red line):

……………………………………………………………………………………………..

Goldman Sachs – Price chart on May 20 (StreetSmart Edge trading platform)

……………………………………………………………………………………………..

What I am looking for is bearish and bullish trends over a longer period. In this case, a death cross (circled in red) occurred in early 2022, a lagging indicator of a bearish price trend.

This trend was reversed in late 2022, indicated by the golden cross (circled in blue), indicating a bullish trend, and followed by another death cross in April 2023.

From that point forward, this stock’s price has been bearish, as you can in the Friday closing price on May 19, and I consider it a buying opportunity while in this bearish range.

My perspective was also reiterated in an August 2022 article in Investopedia:

A death cross signals a bearish market or asset and can be a good time to buy. Many investors purchase assets when the value of those assets has dropped, but with the expectation that the value will go up again in the future, based on their analysis.

Here is a trading scenario. If you look at the chart above, an investor that bought 1 share in Goldman after the death cross of early 2022, at $340, and held on to it until the golden cross of November 2022, selling at $380, would have made a $40 profit, or roughly 12%, in addition to any dividends along the way.

This is a scenario that suits longer term investors willing to hold the stock.

It’s worth noting that it can also mean paper losses / unrealized losses in periods of volatility, since an upward or downward trend lasting any specific time is not guaranteed, so it is another reason why I would go with a dividend paying stock to offset that risk.

In addition, if an investor holds at least 100 shares of the stock and is approved by their brokerage to sell covered call options, that is another income stream they can generate just by holding a stock longer term and generating income in the form of options premiums on the covered calls they sell.

By going long on Goldman, my threefold income strategy includes dividend income, income from covered call premiums, and capital gains after selling the stock at a profit. I call it the triple play.

If you look at the options chain on Seeking Alpha for this stock, for example, a June 2 call option at the strike price of $330 is selling for $3.55. On 1 call option sold, an investor can already snag $355 in options premiums instantly.

A Risk to my Outlook is the Liquidity Risk of Banks

From a forward-looking view, the risk to my positive outlook on Goldman Sachs could be that in the next few quarters it runs into the key risk to the banking sector I already mentioned.. a liquidity risk, or the appearance of one, particularly if a lot of the firm’s clients suddenly decide to pull their money out of the firm, and this is a risk that all banks face actually.

However, let’s keep in mind that the Federal Reserve has various tools in its kit to ensure liquidity to a firm like this, in the case of liquidity issues. On top of that, the Fed launched their new Bank Term Funding Program in March to help the sector as well.

Banks can also lend to each other in the form of overnight loans, through the interbank lending market. This is nothing new, but has been an option for years.

Obviously, these loans are not free and they have the cost of current interest rates, so the cost of debt will be higher than a few years ago, but the point is that these options provide a lifeline if the ship takes on water in the harbor!

As I have shown already, I don’t expect this to be the issue for Goldman, nor do I think they will have the same issue as Silicon Valley Bank of having to sell off a bunch of bonds at a huge loss to cover a run on deposits.

Other risks that I think are more likely, however, could include continued headwinds to its consumer business.

Conclusion

In conclusion, I am reiterating my Buy rating for Goldman Sachs.

In my investing thesis today I showed evidence as to why I am giving it a buy rating: attractive dividends, strong capital position, revenue diversification, and a current price trend that is bearish.. opening the door for buying opportunities before the next upward trend occurs again.

Financial storms will come and go. Much like the storms.. and an occasional hurricane.. that stirs up the waters of New York harbor, my bet is not on the quick-money artists that come and go but the firms that have proven they can lead and manage even in the most difficult times for their sector, not just in the good times.

Source: seekingalpha.com

{kind=link}

{kind=link}

{kind=link}

{kind=link}