emyu

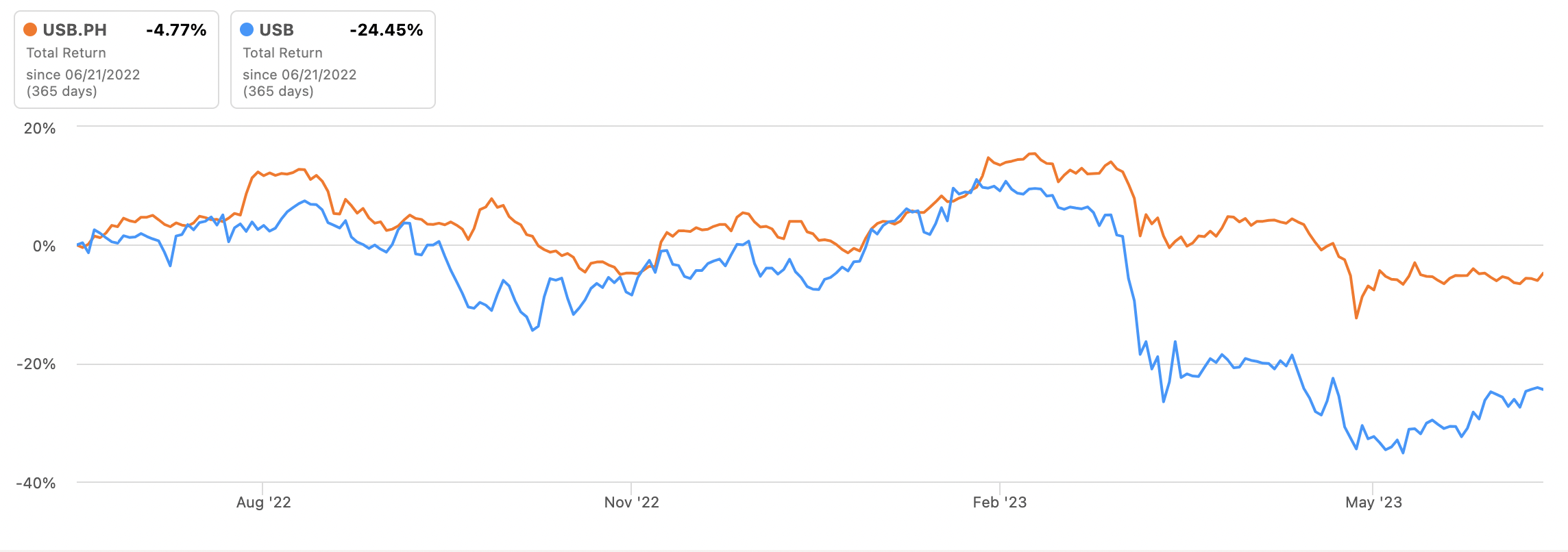

What drives the pricing of preferred stock? The headline coupon rate, the Fed funds rate, and the perceived strength of the underlying company. Hence, whilst the 7% decline in the value of U.S. Bancorp Floating Rate Series B Preferred Stock (USB.PH) is understandable against ten consecutive interest rate hikes up until the June pause, its continued weakness has opened up an opportunity to accumulate shares in the security at a marked discount to par value and against a floating yield that could move to double-digits. There’s a lot to like here from the fifth largest banking institution in the US whose commons are yet to recover from the March banking panic.

QuantumOnline

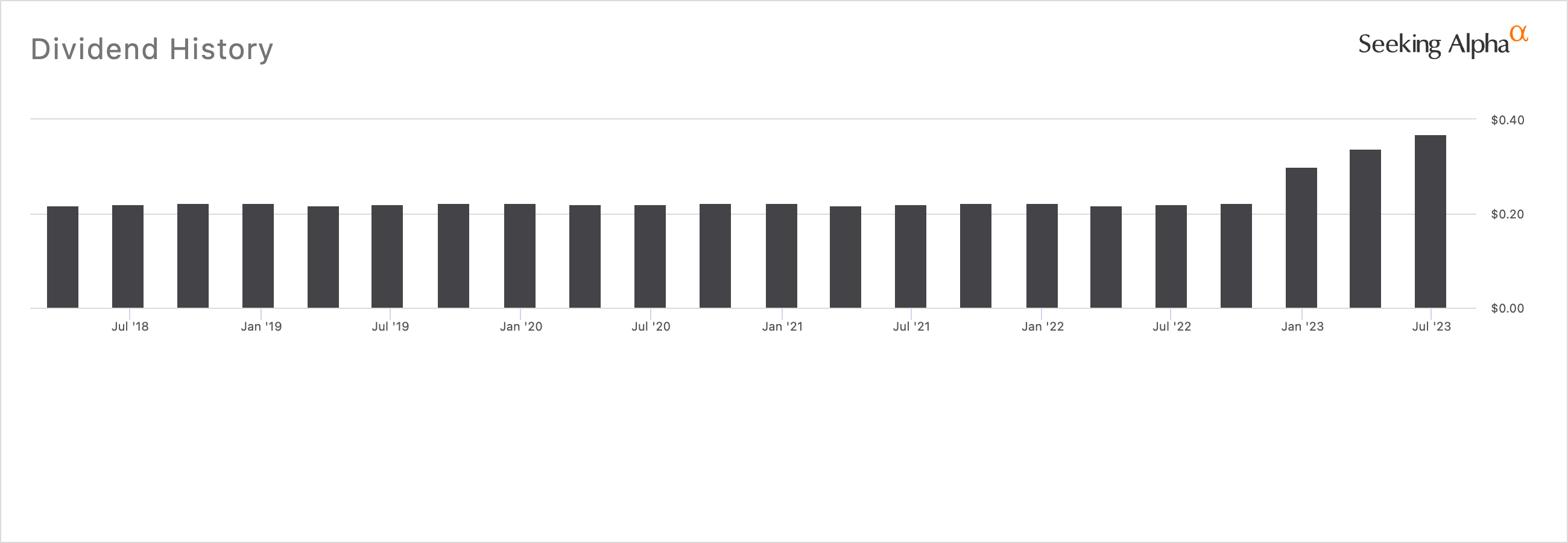

Firstly, the Series B preferreds pay out a variable rate equal to 0.60% above the three-month LIBOR. Hence, they last declared a quarterly coupon of $0.37 per preferred share, an increase of $0.03 over the prior quarter and for an 8.4% forward annualized yield on cost. This forward yield could be an understatement with the current three-month LIBOR at 5.5% likely to move higher if the Fed follows up with statements that more rate hikes are likely this year. Whilst I don’t think this will happen as inflation data continues to trace its way back to the Fed’s 2% target, the holders of the Series B are in a strong position where any downward pricing of the preferreds as a result of rising rates has been countered by a surging variable yield.

Seeking Alpha

The Upside Potential

Further, the preferreds are currently swapping hands for $17.70 per share, a $7.30 difference from their $25 par value. This 29% discount to par essentially means you’re able to buy these for 71 cents on the dollar. Critically, it forms further upside to be captured as you get paid a growing coupon to wait for it to move back to par. However, a move back to par is very unlikely without a total normalization of interest rates and inflation. Hence, there is somewhat of an inherent contradiction with these as a move back to par is predicated on interest rates falling which would in turn drive down the floating rate. This floating rate is subject to a 3.5% floor.

Seeking Alpha

The common shares are down 24.5% over the last year on the back of the March banking panic sparked by the failure of Silicon Valley Bank. These also pay out a dividend with the bank last declaring a quarterly dividend payout of $0.48 per share, in line with its prior payment and for a 5.7% annualized forward dividend yield. Whilst this is 265 basis points lower than the current yield on the preferreds, I think the commons possess an overall greater upside potential from their current level. The panic here is centered on the flows of both insured and uninsured banking deposits as the landscape of US banking looks set to be shaped by a flight of deposits to more systematically important banks like Wells Fargo (WFC), Bank of America (BAC), JPMorgan Chase (JPM), and Citi (C).

Deposits And Net Interest Margin Grow

U.S. Bancorp remains in a position of strength even with Moody’s downgrading its credit rating to the fourth-lowest investment grade rating. The company recorded fiscal 2023 first-quarter revenue of $7.18 billion, an increase of 28.2% over its year-ago comp and a beat by $50 million on consensus estimates. This came on the back of a net interest margin that expanded sequentially by 9 basis points over the fourth quarter to 3.1%. Critically, the company recorded an average deposit growth of 12.4% over its year-ago quarter and sequential growth of 5.9% over the fourth quarter. Of course, the operating environment has markedly deteriorated over its year-ago comp to warrant the discount, but bulls have a recovery in view for both the commons and preferreds to their pre-March levels if net interest margin and deposits continue to expand.

The preferreds started trading in 2006, two years before the financial crisis, and are currently rated Baa2 which is medium grade. They’re non-cumulative, but the likelihood of a coupon suspension is near-zero. The coupon payments were maintained through the 2008 financial crisis, the pandemic crash, and the March banking crisis. Describing a security as nearly risk-free is not entirely prudent, these have a favorable risk and reward profile. The bank has also seen relatively heavy insider buying over the last three months with 76,698 common shares bought and none sold to perhaps underlie the confidence in the recovery of the bank. I like the preferreds here against their larger yield and marked discount to par. More adventurous investors are likely best served to go with the commons with the March banking panic discount unlikely to last over the medium term. The preferreds offer more stability and a rising floating yield that forms a strong hedge against any possible upside inflation surprises.

Source: seekingalpha.com

{kind=link}

{kind=link}

{kind=link}