Brandon Bell

Consumers keep spending, but excess savings are virtually gone. While August retail sales verified better than what economists were expecting as real wages continue in positive territory, there’s a real threat of a spending slowdown which could hurt consumer-facing financial institutions. Any mild downturn in the jobs’ situation could break consumers’ back, however. As banks increase their credit reserves and as investors pour cash into money market funds from checking accounts, diversified banks have a set of risks and opportunities.

I have a hold rating on Bank of America Corporation (NYSE:BAC). I like the valuation and yield, but a soft growth outlook, macro risks, and downright poor price action say hold off for now.

All signs point to a retreat in consumption in the months ahead

The Daily Shot

For background, Bank of America Corporation provides banking and financial products and services for individual consumers, small and middle-market businesses, institutional investors, large corporations, and governments worldwide. It has Consumer Banking, Global Wealth & Investment Management, Global Banking, and Global Markets segments.

The Charlotte-based $232 billion market cap Diversified Banks industry company within the Financials sector trades at a low 8.4 trailing 12-month GAAP price-to-earnings ratio, a very low 0.9 trailing price-to-book ratio, and a forward dividend yield of 3.3%. Ahead of earnings next month, the stock features an implied volatility percentage of 19% while its short interest is also modest at just 0.7% as of September 14, 2023.

Back in July, BofA issued a solid Q2 earnings report. EPS verified at $0.88, topping estimates by a nickel, while revenue rose 3% year-on-year to $25.2 billion, also a modest beat. Earnings were down from the same quarter a year ago, but were also up sequentially. The beat was attributed to the robust performance of its Global Banking unit, while net interest income was near expectations and non-interest income stood at $11.0 billion, above estimates with YoY growth. Troubling was its $1.13 billion rise in provisions for credit losses – about double that of Q2 2022’s $571 million figure.

Concerning, however, is that BofA’s high exposure to the US consumer could be a risk as the year progresses and as uncertainty with 2024 approaches. A month ago, it was reported that credit card delinquencies notched their highest mark since before the pandemic. Households’ excess savings built up in 2020 and 2021 are largely gone as inflation runs above long-term averages, and that comes despite a healthy jobs market and improved household net worth trends. Further deterioration in the consumer is a major risk for BofA. Still, the company itself reported a steady charge-off rate for July. Overall, Q2 earnings were pretty good in my view, boosted by solid Global Banking results, with the bank citing improved market share across some segments, particularly in sales and trading and investment banking businesses.

Further regulations are another possible threat to profitability for the big banks, however. News of higher capital requirements could result in a build-up of credit loss reserves, which would hurt near-term profitability. Of course, investors fleeing low-interest-rate checking and savings accounts for money market funds is a risk to the firm’s net interest margin, too. Still, BAC raised its dividend after its earnings report in July – a healthy sign for investors.

With a diversified business portfolio, strong scale and market presence, robust technological infrastructure, and a generally safe capital position, the firm has a wide moat that should persist over the coming market cycles. Moreover, under the leadership of CEO Brian Moynihan, the bank has made significant strides in improving its operations, risk management, and profitability. I expect it to continue to hold a strong position in the banking industry.

On valuation, $3.30 of next-12-month EPS is expected. If we apply the stock’s 5-year average forward operating earnings multiple of 11.8, then shares should be near $39. We can discount that by 10% to 20% to account for higher interest rates, but even that discount yields an undervalued stock. Also, with a typical price-to-book ratio of 1.14, shares look to the cheap side by 20% on that metric.

Stagnant earnings growth ahead

Seeking Alpha

BAC: Cheap across valuation metrics

Seeking Alpha

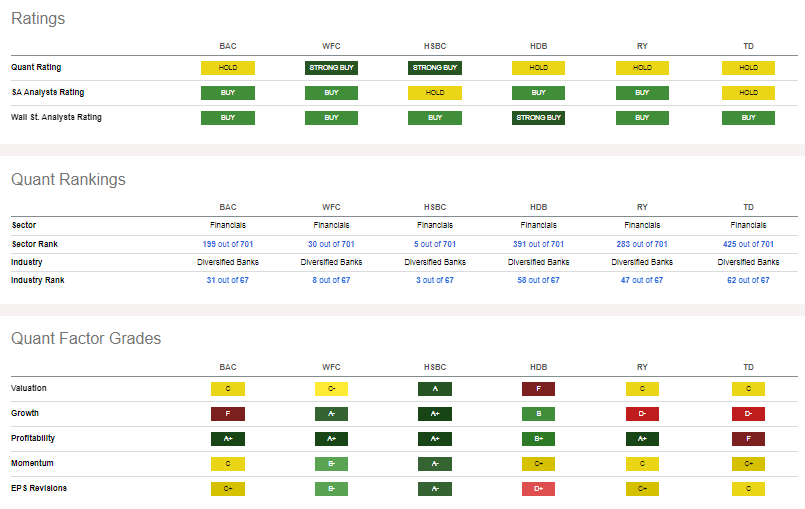

Compared to its peers, BofA may not be the best of the bunch. The growth outlook is most concerning, as Wall Street does not expect a clear path to better earnings in the coming quarters. Still, BAC earns a pristine A+ profitability rating while share-price momentum and EPS Revisions are more lackluster, but that is common among large diversified domestic banks.

Competitor analysis

Seeking Alpha

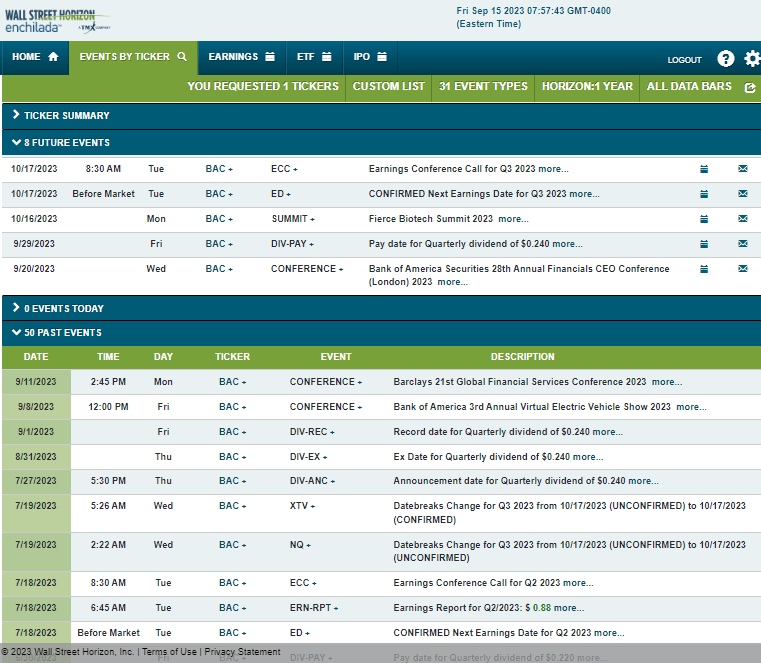

Looking ahead, corporate event data provided by Wall Street Horizon show a confirmed Q3 2023 earnings date of Tuesday, October 17, BMO with a conference call immediately after the results cross the wires. You can listen live here. Before the reporting date, the management team is slated to present at a pair of industry conferences. The first is the Bank of America Securities 28th Annual Financials CEO Conference from September 19 to 21 and the second is the Fierce Biotech Summit 2023 from October 16 to 18.

Corporate event risk calendar

Wall Street Horizon

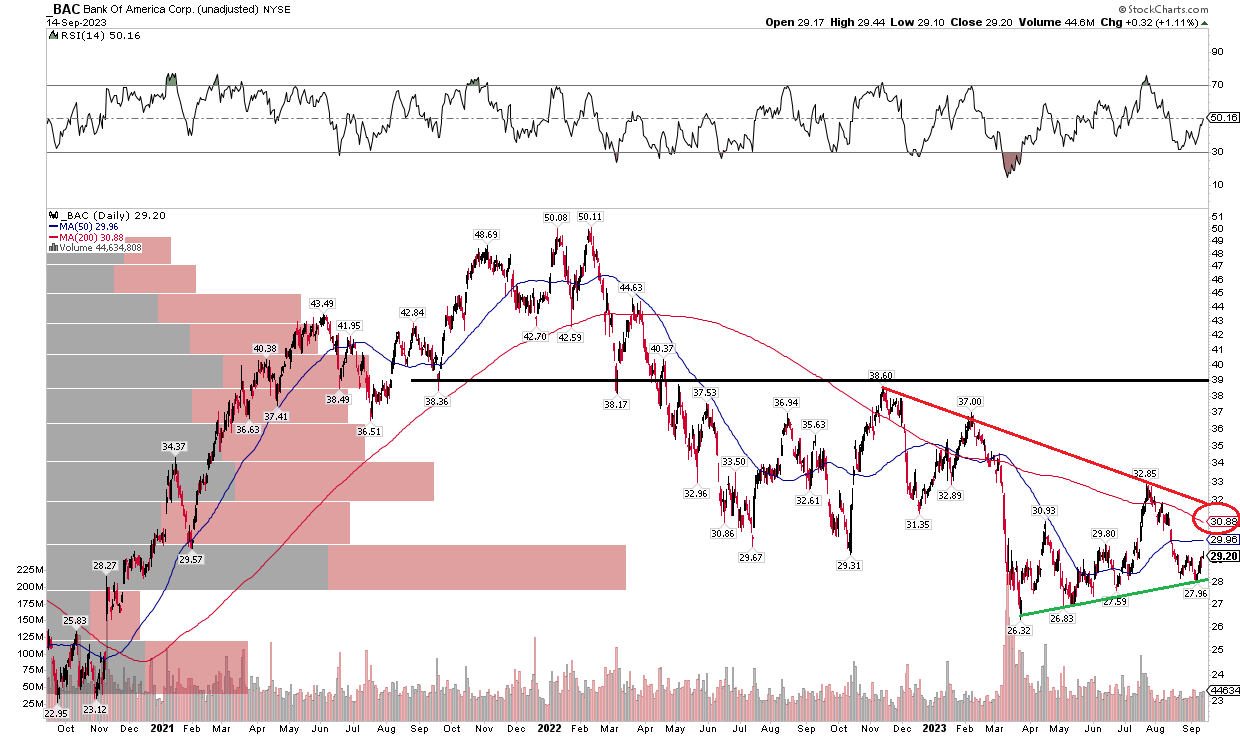

The Technical Take

BAC has been a major underperforming stock since early last year. After peaking above $50 in Q1 2022, the stock is down more than 35% on a total return basis, sharply under the S&P 500’s modest loss and the Financials sector’s 12% drop over the last 20 months. Notice in the chart below that shares are also mired in a more recent downtrend off a near-term high just shy of $39 in Q4 last year.

While the SPX has continued its ascent, BAC has fallen. With a negatively sloped 200-day moving average, the bears appear in control while a series of lower highs continues. What’s encouraging, though, is that since mid-March, there have been higher lows. Thus, there is a consolidation pattern here, but that’s happening within a broader downtrend. The assertion is that the next move will be down, since that is the trend of larger degree. I see upside resistance in the $38 to $39 range, while a broad area of possible support is from the March nadir of $26.32 to the September low of $27.96.

Overall, it is a bearish chart, and I would like to see BAC climb above the July peak and 200dma to help confirm a bullish reversal.

BAC: Bearish consolidation, falling 200dma, eyeing the March low

Stockcharts.com

The Bottom Line

I have a hold rating on BAC. The valuation is attractive on an earnings and P/B basis, but the chart is too concerning right now with poor momentum as consumer strength appears to be waning.

Source: seekingalpha.com

{kind=link}

{kind=link}

{kind=link}