In the evolving regional banking sector, Truist Financial (TFC) has emerged as a case study in post-merger adaptation. Since its 2019 consolidation of SunTrust and BB&T, the bank has navigated a landscape marked by technological disruption, regulatory scrutiny, and shifting consumer preferences. As of Q2 2025, Truist’s financial performance and strategic initiatives suggest a resilient but cautiously optimistic outlook.

Profitability: Strong Metrics, Room for Caution

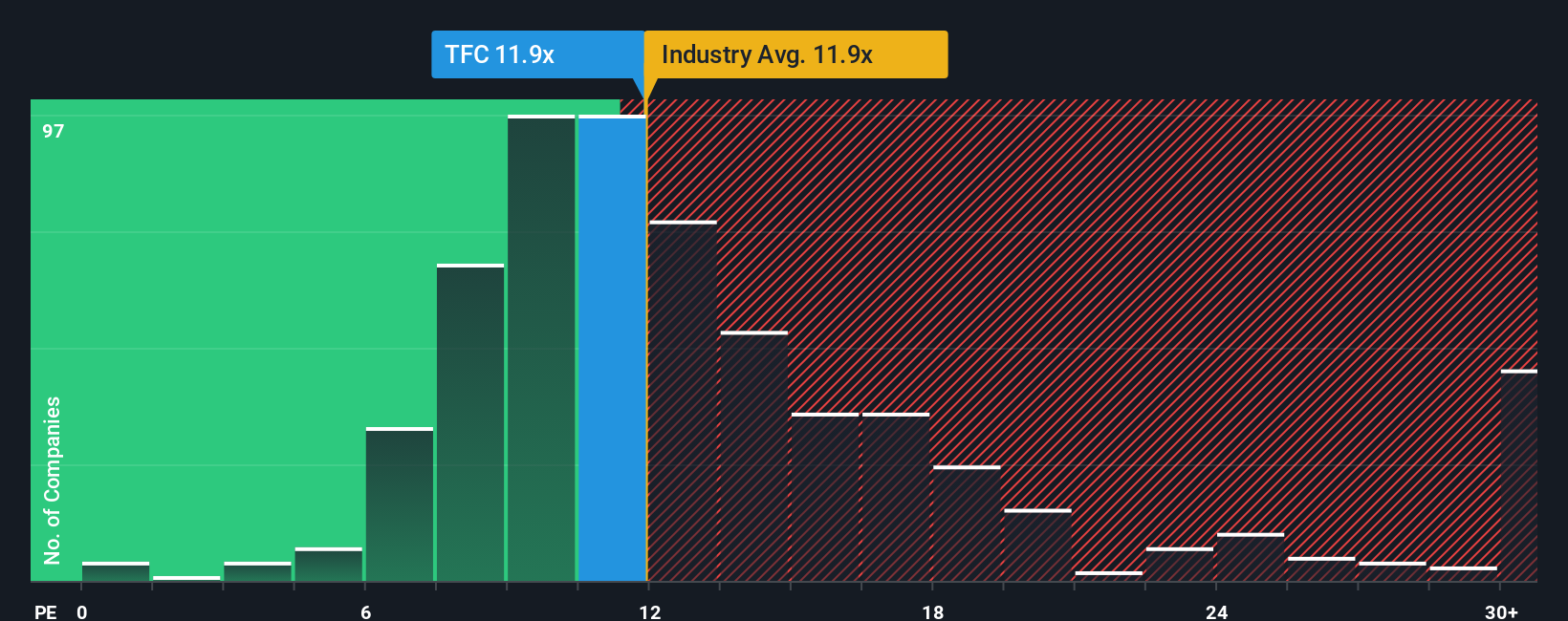

Truist’s Q2 2025 earnings report highlights robust profitability. Net income of $1.2 billion, or $0.90 per share, reflects a Return on Common Equity (ROCE) of 8.1% and a Return on Tangible Common Equity (ROTCE) of 12.3% [3]. These figures outpace its 2024 ROTCE of 10.4% and align with industry benchmarks, where the average efficiency ratio hovers near 60% [3]. Truist’s adjusted efficiency ratio of 57.1% underscores disciplined expense management, though the unadjusted ratio of 59.9% signals rising personnel costs [3].

The bank’s capital position remains a strength, with a CET1 ratio of 11.0%, well above the 7% regulatory minimum [3]. Share repurchases of $750 million and a 121% payout ratio further demonstrate confidence in its valuation. However, the efficiency ratio’s slight uptick from the prior quarter raises questions about sustainability amid inflationary pressures.

Strategic Positioning: Digital Innovation and Geographic Expansion

Truist’s post-merger strategy has focused on high-growth markets and digital transformation. Its 3.09% market share in the U.S. commercial banking sector [2] places it among the top regional players, though it trails industry giants like JPMorgan Chase (29.19%) and Bank of America (18.63%) [2]. Sequential loan growth of 3.3% in Q2 2025, driven by commercial and industrial (C&I) lending, reflects its focus on manufacturing hubs and tech corridors [6].

Digital initiatives have been a cornerstone of its strategy. Truist’s AI-driven Truist Insights platform delivers 550 million personalized financial insights annually, while digital account production grew 17% year-over-year [6]. These efforts have reduced acquisition costs and enhanced customer engagement. The bank also plans to open 100 new “insights-driven” branches and renovate 300 more in cities like Atlanta and Charlotte [4].

However, the merger’s legacy includes 820 branch closures, sparking criticism about reduced access in low-income and diverse communities [5]. While Truist claims to avoid such closures and has pledged $60 billion in community investments, advocacy groups argue new branches disproportionately favor higher-income areas [5].

Challenges: Deposit Volatility and Cost Pressures

Despite its strengths, Truist faces headwinds. A $10.9 billion withdrawal of short-term client deposits in Q2 2025 has raised concerns about funding costs and deposit beta [6]. Rising personnel expenses have also pushed the efficiency ratio higher, challenging the bank’s cost discipline.

The broader regional banking sector is grappling with consolidation and regulatory pressures. Deutsche Bank’s CET1 ratio of 14.2% [2]—well above Truist’s—highlights the capital buffers some peers maintain. For Truist, balancing growth with capital returns (a 100% payout ratio in Q2 2025 [6]) will be critical to sustaining shareholder value.

Conclusion: A Model for Regional Banking?

Truist’s post-merger trajectory offers a mixed but compelling narrative. Its profitability metrics and digital innovation position it as a leader in regional banking, while geographic expansion and capital returns reinforce long-term value creation. Yet deposit volatility, rising costs, and community access concerns underscore the sector’s inherent risks.

For investors, Truist represents a bet on a bank that has successfully navigated consolidation but must now prove its ability to adapt to a digital-first, low-margin environment. The coming quarters will test whether its strategic pillars—loan growth, digital transformation, and capital returns—can sustain its resilience.

Source:

[1] Truist Financial Corp Reports Q1 2025 Earnings [https://www.gurufocus.com/news/2785921/truist-financial-corp-reports-q1-2025-earnings-eps-meets-estimates-at-087-revenue-surpasses-expectations-at-495-billion][2] TFC’s Market Share Relative to Its Competitors, as of Q2 2025 [https://csimarket.com/stocks/competitionSEG2.php?code=TFC][3] Average loans increased $6.2 billion, or 2.0% [https://www.sec.gov/Archives/edgar/data/92230/000009223025000118/ex991-pr2q25.htm][4] Truist Announces Significant Multi-Year Investment in High-Growth Markets [https://ir.truist.com/2025-08-20-Truist-announces-significant-multi-year-investment-in-high-growth-markets][5] Truist opening fewer branches in diverse areas, group claims [https://www.charlotteobserver.com/news/business/banking/article257093337.html][6] Truist Financial’s Q2 2025: A Blueprint for Regional Banking Resilience [https://www.ainvest.com/news/truist-financial-q2-2025-blueprint-regional-banking-resilience-2507/]

Source: ainvest.com