- In early November 2025, U.S. Bancorp announced the launch of the U.S. Bank Split™ World Mastercard® credit card, which automatically converts all purchases into equal no-fee, no-interest monthly payments, and expanded its partnership with Edward Jones to offer co-branded banking solutions to millions of new clients.

- This rollout highlights U.S. Bancorp’s push into innovative, flexible digital payment products and new distribution channels in collaboration with major financial advisors.

- We’ll explore how the introduction of automatic pay-over-time credit cards could shape U.S. Bancorp’s investment narrative moving forward.

The end of cancer? These 29 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer’s.

Advertisement

U.S. Bancorp Investment Narrative Recap

To own U.S. Bancorp stock, an investor typically needs confidence in its ability to grow fee-based revenues and control costs amid fierce digital competition and shifting consumer banking preferences. The recent launch of the Split™ World Mastercard® offers a modern twist on digital lending, but it does not materially alter the most pressing short-term catalyst: sustaining momentum in payment volumes and digital fee income. The main risk remains exposure to new fintech competitors that could erode traditional income streams.

The expansion of co-branded banking solutions through Edward Jones stands out as particularly relevant, as it increases U.S. Bancorp’s reach into a broader client base and may support continued growth in core deposit and lending activities, both important for driving net interest income and earnings.

Yet, while these moves may support revenue, investors should be aware that competition from digital-first challengers could…

Read the full narrative on U.S. Bancorp (it’s free!)

U.S. Bancorp’s outlook anticipates $32.6 billion in revenue and $7.4 billion in earnings by 2028. This projection is based on an 8.5% annual revenue growth rate and an increase in earnings of $0.9 billion from the current $6.5 billion.

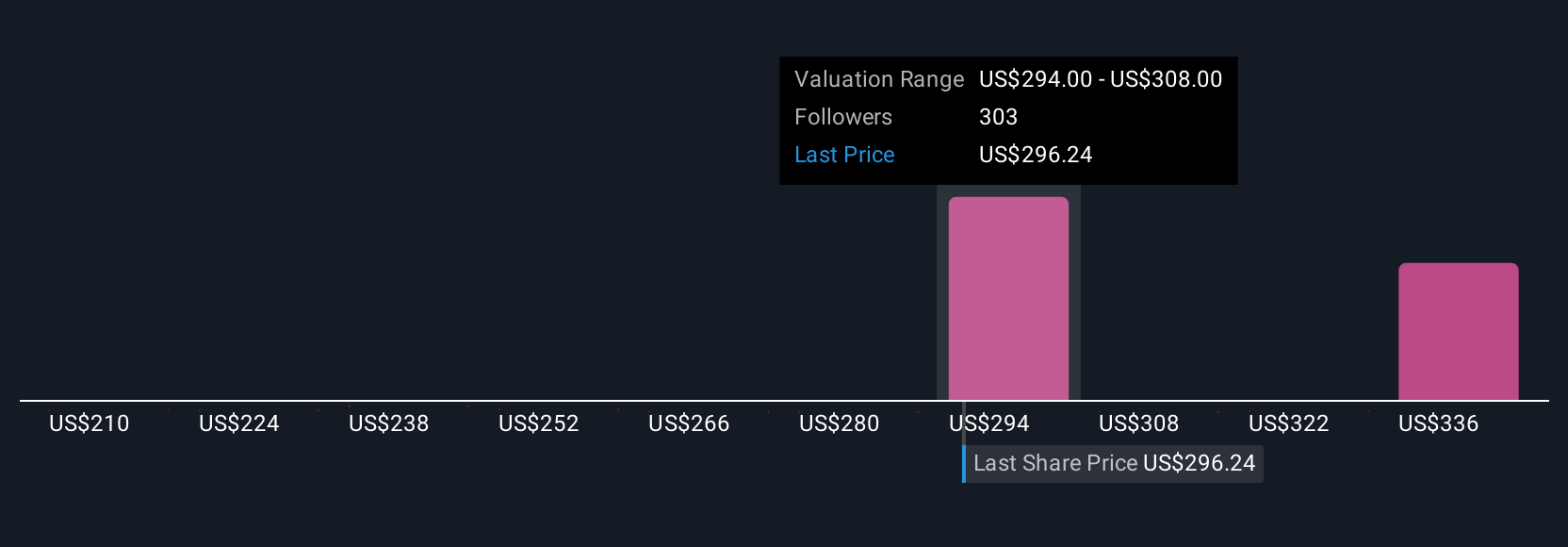

Uncover how U.S. Bancorp’s forecasts yield a $55.72 fair value, a 19% upside to its current price.

Exploring Other Perspectives

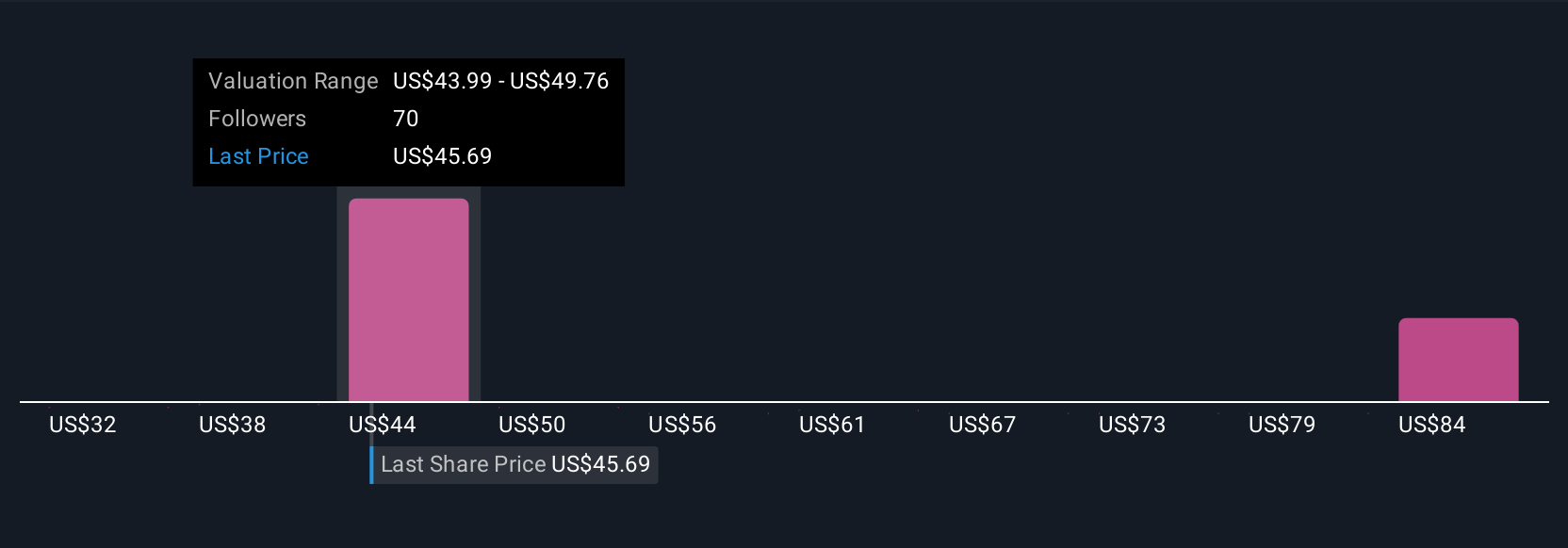

Simply Wall St Community members have published nine fair value estimates for U.S. Bancorp ranging widely from US$35 to US$84. This diversity in opinion comes as many highlight growth in payments and digital banking as a core catalyst for the company’s future, underscoring the importance of reviewing a range of viewpoints before making decisions.

Explore 9 other fair value estimates on U.S. Bancorp – why the stock might be worth 25% less than the current price!

Build Your Own U.S. Bancorp Narrative

Disagree with existing narratives? Create your own in under 3 minutes – extraordinary investment returns rarely come from following the herd.

- A great starting point for your U.S. Bancorp research is our analysis highlighting 5 key rewards that could impact your investment decision.

- Our free U.S. Bancorp research report provides a comprehensive fundamental analysis summarized in a single visual – the Snowflake – making it easy to evaluate U.S. Bancorp’s overall financial health at a glance.

Contemplating Other Strategies?

These stocks are moving-our analysis flagged them today. Act fast before the price catches up:

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Source: simplywall.st