- Wells Fargo recently announced a series of senior unsecured note offerings with varying maturities and coupon rates, as well as an increase in its quarterly dividend to US$0.45 per share, payable in September 2025 to shareholders of record as of August 8, 2025.

- This move, alongside ongoing capital management initiatives, highlights the company’s efforts to optimize its funding structure while demonstrating confidence in future earnings and shareholder returns.

- We’ll assess how Wells Fargo’s dividend increase and multiple new bond offerings influence its growth outlook and capital efficiency story.

AI is about to change healthcare. These 26 stocks are working on everything from early diagnostics to drug discovery. The best part – they are all under $10b in market cap – there’s still time to get in early.

Advertisement

Wells Fargo Investment Narrative Recap

To own Wells Fargo stock right now, you need to believe in the company’s ability to grow earnings and improve efficiency as it unlocks its balance sheet, all while carefully managing its cost base in a very competitive and evolving financial sector. Recent news about multiple senior note offerings and a dividend increase reinforce Wells Fargo’s focus on capital management but have limited impact on the near-term catalyst, which continues to be cost control and efficient deposit growth, while persistent regulatory requirements remain the leading risk to watch.

Among recent announcements, the new collaboration with the National Center for the Middle Market stands out. This partnership may help Wells Fargo tap deeper into the US middle market segment, which is a vital source of lending and fee income, positioning the bank for growth, an important catalyst as it seeks to offset margin pressures and competitive threats.

However, despite these positives, investors should also be mindful that, unlike the optimism surrounding capital initiatives, ongoing regulatory obligations continue to…

Read the full narrative on Wells Fargo (it’s free!)

Wells Fargo’s outlook anticipates $90.9 billion in revenue and $22.1 billion in earnings by 2028. This scenario assumes a 5.4% annual revenue growth and a $2.6 billion increase in earnings from the current $19.5 billion.

Uncover how Wells Fargo’s forecasts yield a $86.96 fair value, a 12% upside to its current price.

Exploring Other Perspectives

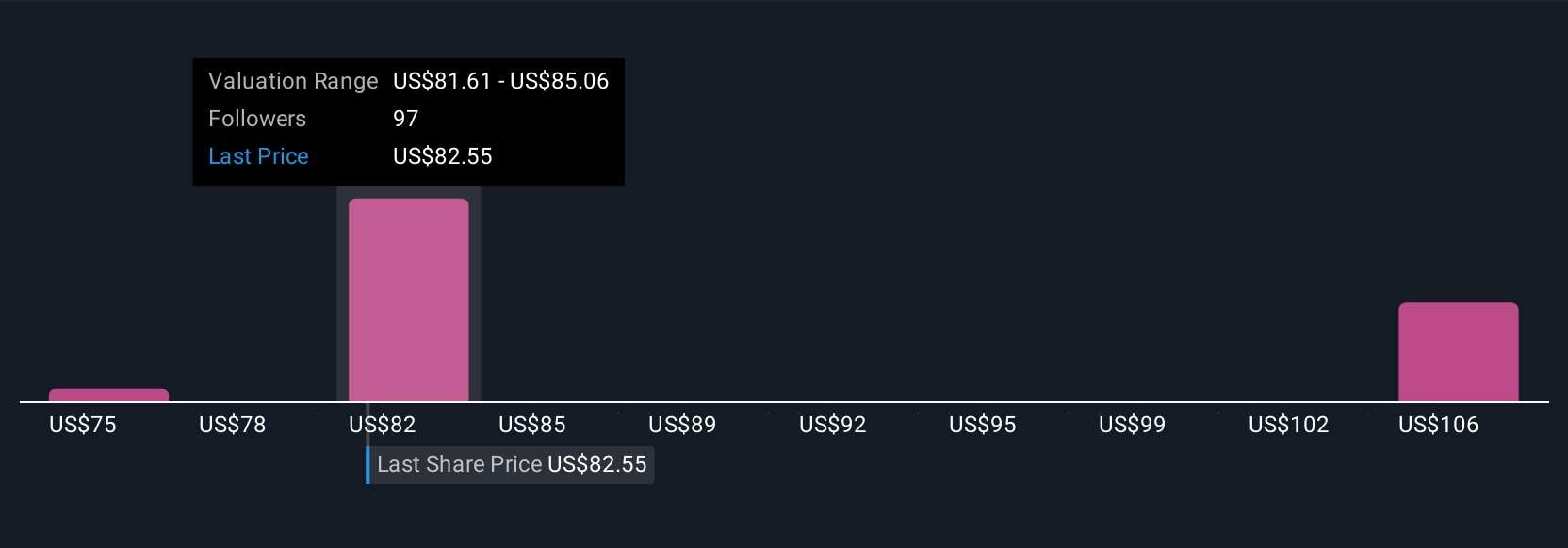

Simply Wall St Community members’ fair value estimates for Wells Fargo range from US$74.70 to US$100.33, with four distinct perspectives reflecting wide variance. While many see long-term opportunity as earnings growth resumes, sustained regulatory challenges could weigh on efficiency and future returns, reminding you that consensus can overlook key risks and warrant broader consideration.

Explore 4 other fair value estimates on Wells Fargo – why the stock might be worth just $74.70!

Build Your Own Wells Fargo Narrative

Disagree with existing narratives? Create your own in under 3 minutes – extraordinary investment returns rarely come from following the herd.

Seeking Other Investments?

The market won’t wait. These fast-moving stocks are hot now. Grab the list before they run:

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we’re here to simplify it.

Discover if Wells Fargo might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Source: simplywall.st