- Oppenheimer recently upgraded PNC Financial Services Group to “Outperform,” citing the bank’s consistent profitability, strong management, and accelerating customer acquisition, even amid economic uncertainties.

- The entry of Cullen Capital Management as an investor reflects growing institutional confidence in PNC’s business expansion following its acquisition of BBVA’s US operations.

- We’ll explore how Oppenheimer’s positive assessment of PNC’s management and growth strategy could influence its investment outlook going forward.

Find companies with promising cash flow potential yet trading below their fair value.

Advertisement

PNC Financial Services Group Investment Narrative Recap

To hold PNC Financial Services Group stock, you need confidence in the bank’s ability to drive stable earnings growth through disciplined management and organic customer acquisition, despite economic uncertainty and industry volatility. Oppenheimer’s upgrade and increased institutional interest signal that confidence, but the biggest short term catalysts, such as sustained net interest income growth and expense control, remain largely unchanged, while the biggest risk continues to be the unpredictable impact of macroeconomic conditions on noninterest income.

Among recent company announcements, PNC’s Q2 2025 earnings update is highly relevant. The bank reported year-over-year increases in both net interest income and net income, reflecting its focus on core fundamentals and hinting at the importance of maintaining growth momentum as a key catalyst for future performance.

On the other hand, investors should keep in mind risks related to capital markets fee volatility, as…

Read the full narrative on PNC Financial Services Group (it’s free!)

PNC Financial Services Group is projected to reach $24.5 billion in revenue and $6.5 billion in earnings by 2028. This outlook is based on an assumed annual revenue growth rate of 4.9% and reflects a $0.7 billion increase in earnings from the current $5.8 billion.

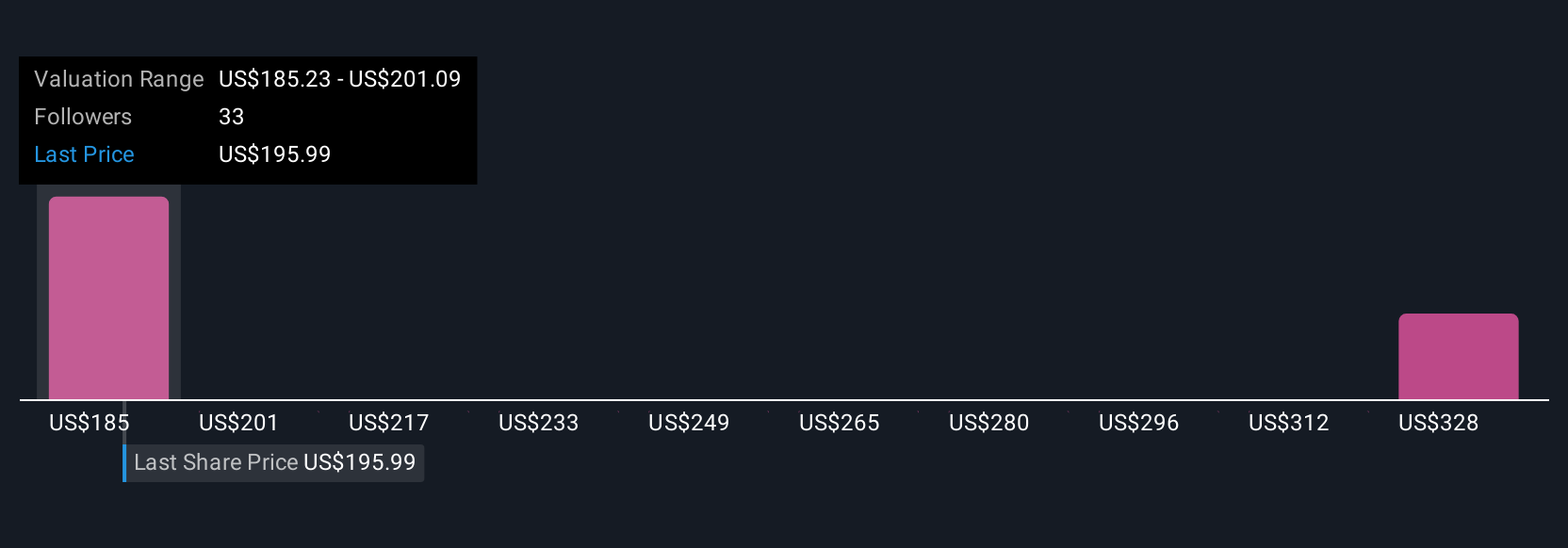

Uncover how PNC Financial Services Group’s forecasts yield a $214.15 fair value, a 13% upside to its current price.

Exploring Other Perspectives

Simply Wall St Community members posted four fair value estimates for PNC ranging from US$179.10 up to US$317.75 per share. In light of recent institutional optimism, the ongoing uncertainty in noninterest income highlights why these opinions diverge and make it valuable to explore different views.

Explore 4 other fair value estimates on PNC Financial Services Group – why the stock might be worth 6% less than the current price!

Build Your Own PNC Financial Services Group Narrative

Disagree with existing narratives? Create your own in under 3 minutes – extraordinary investment returns rarely come from following the herd.

No Opportunity In PNC Financial Services Group?

Early movers are already taking notice. See the stocks they’re targeting before they’ve flown the coop:

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We’ve created the ultimate portfolio companion for stock investors, and it’s free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Source: simplywall.st