Advertisement

Bank of America stock after recent performance

Bank of America (BAC) shares have been relatively steady over the past month, with a small decline compared with a modest gain over the past 3 months. This helps put recent moves into a broader context for investors.

See our latest analysis for Bank of America.

At around US$52.55, Bank of America’s recent share price moves show some cooling in short term momentum, with a 7 day share price return of a 7.04% decline. However, longer term total shareholder returns of 14.5% over one year and 71.7% over five years point to a materially different experience for investors who stayed invested.

If this has you thinking about how financial exposure fits into your portfolio, you might also want to scan for opportunities in companies tied to power and infrastructure upgrades using our 25 power grid technology and infrastructure stocks as a starting point.

So with Bank of America trading at about US$52.55 and screens suggesting roughly a 19% intrinsic discount, is the recent pullback a chance to buy, or is the market already pricing in the bank’s future growth?

Most Popular Narrative: 21.3% Overvalued

According to the most widely followed narrative, Bank of America’s fair value sits at $43.34, which is below the recent $52.55 share price and presents a clear valuation gap for you to weigh.

Despite economic uncertainties, BAC has a resilient loan book and solid profit margins, which may help it navigate potential challenges.

BAC’s valuation appears attractive relative to peers, but the broad sector is vulnerable to swift interest rate changes.

Curious about the revenue mix and profit margins behind that valuation gap? The narrative focuses on steady loan growth, disciplined costs and a modest profit multiple to support its view. Want to see exactly how those moving parts add up in the model?

Result: Fair Value of $43.34 (OVERVALUED)

Have a read of the narrative in full and understand what’s behind the forecasts.

However, you still need to weigh risks such as a sharp economic downturn hurting loan quality, or heavier regulation that could pressure Bank of America’s profitability and valuation.

Find out about the key risks to this Bank of America narrative.

Another View: Multiples Point to a Different Story

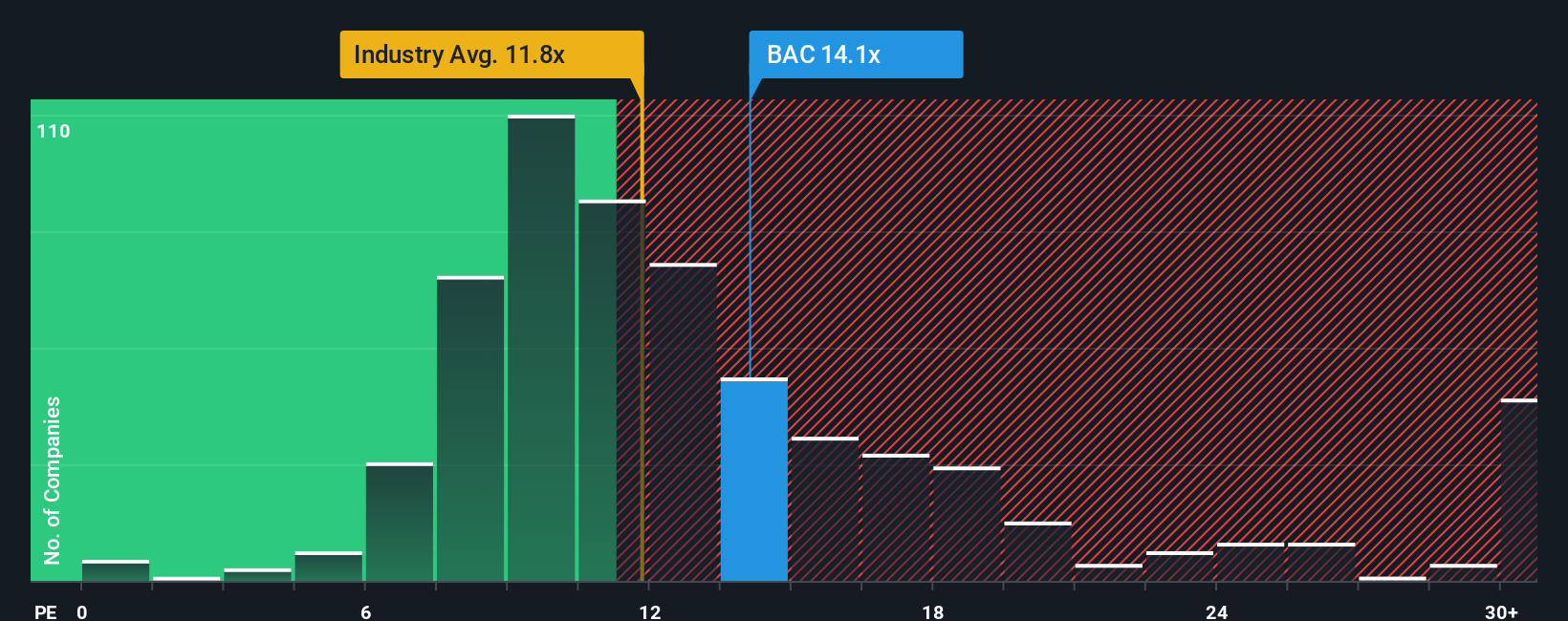

The most popular narrative pegs fair value at $43.34, which sits below the current $52.55 price. Yet our P/E work presents a different perspective. Bank of America trades at 13x earnings, compared with a fair ratio of 16.5x and a peer average of 13.8x, while the broader US banks industry sits lower at 11.9x.

In plain terms, the stock carries a small premium to the industry but still sits below both peers and the fair ratio. Investors may view that gap as either potential valuation risk or a possible margin of safety.

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Bank of America Narrative

If you see the numbers differently or prefer to lean on your own work, you can build a complete valuation story yourself in just a few minutes: Do it your way.

A good starting point is our analysis highlighting 4 key rewards investors are optimistic about regarding Bank of America.

Looking for more investment ideas?

If you stop at one stock, you limit your options. Use these screeners to quickly spot other opportunities that fit different roles in your portfolio.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we’re here to simplify it.

Discover if Bank of America might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Source: simplywall.st