Too-high prices destroy demand. Everyone knows that. Lower prices would bring out demand.

By Wolf Richter for WOLF STREET.

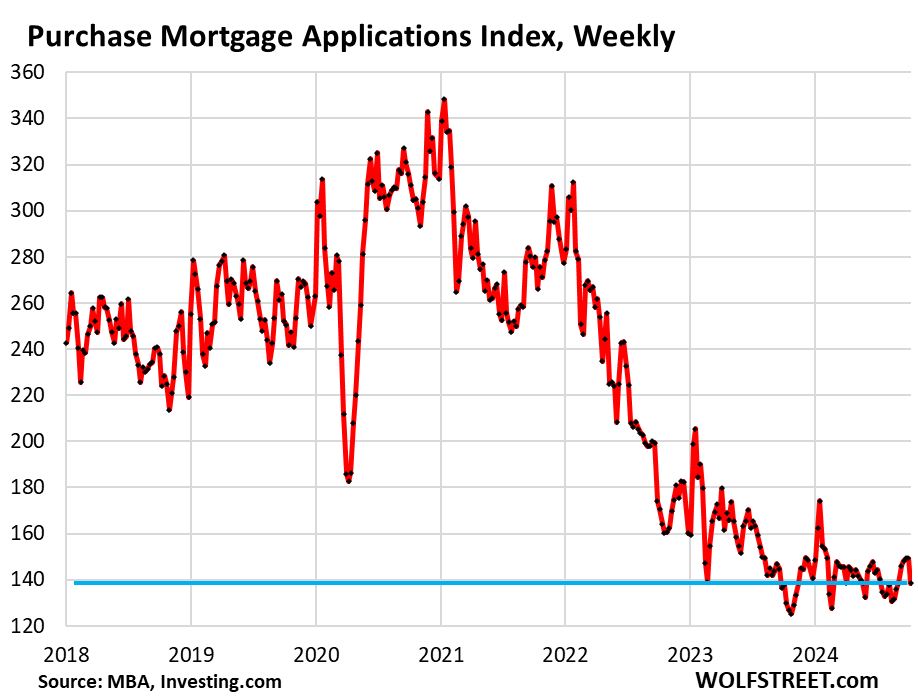

The extent to which demand for existing homes has collapsed and remains collapsed is astounding, but ultimately not surprising: Demand plunged in 2022 when mortgage rates soared, and plunged a lot further in 2023 as mortgage rates continued to rise to almost 8% by October 2023. But then as mortgage rates dropped starting in November, and kept dropping in 2024, demand stayed at these collapsed levels through September, despite mortgage rates having dropped to near 6%. And now that mortgage rates have bounced off the September lows since the rate cut, demand has collapsed further, even as inventories have been rising all year (look below the article at the top of the comments for inventory and supply charts of existing homes and new houses).

And everyone knows why: Prices are too high. That prices are too high, after the crazy spike, can be seen in the charts of our Most Splendid Housing Bubbles in America. And people have gone on Buyers’ Strike. We’ve been saying that for a long time, and Fannie Mae found in a survey just before the rate cut that lower prices are exactly what buyers are waiting for – lower prices, lower mortgage rates, and higher wages. In other words, people are still on Buyers’ Strike, and they’re staying on strike.

And it was confirmed today by the plunge in weekly applications for mortgages to purchase a home – a plunge from already historically low levels – according to data from the Mortgage Bankers Association. The Purchase Mortgage Applications Index has stayed in the same historically low range since the beginning of 2023:

Fannie Mae economists, in their forecast for the remainder of 2024 said, “we expect affordability to remain the primary constraint on housing activity for the foreseeable future, and we now think full-year 2024 will produce the fewest existing home sales since 1995.” So we’re not alone.

Sales of existing single-family houses, townhouses, condos, and co-ops have plunged by about 26% from 2018 and 2019, and by about 34% from 2021, according to data from the National Association of Realtors. In 2023, they fell to 4.09 million homes, the lowest since 1995. In 2024 so far through August, sales are tracking 2.5% below 2023. And if that decline continues, sales will drop to about 4.0 million homes.

This demand destruction is worse than it was during the depth of the Financial Crisis as millions of people lost their jobs and mortgages blew up, and 2024 is the second year in a row, all because prices are too high. High prices destroy demand. Everyone knows that (light-blue column = our estimate for 2024, historical data from YCharts).

Mortgage rates had dropped to 6.13% just before the rate cut on September 18, a two-year low, according to Mortgage Bankers Association data. But 11 days after the Fed cut its policy rates by 50 basis points, all data-heck broke loose. Large upward revisions of job growth, personal income, the savings rate, economic growth, and PPI inflation, topped off by CPI inflation rising for the third month in a row, changed the entire scenario, rekindling inflation fears. The bond market reacted to it and longer-term yields surged, as did mortgage rates.

The average 30-year fixed mortgage rate jumped to 6.52% in the latest week, according to the Mortgage Bankers Association today. It’s quite a U-turn:

As mortgage rates dropped from November 2023 through mid-September 2024, home sales have continued to wobble along historic lows. Now that mortgage rates have jumped, home sales will likely fizzle further for the rest of the year.

During the time that mortgage rates dropped, while home sales wobbled along historic lows, applications to refinance existing mortgages rose from the ashes and more than tripled by mid-September, from near-nothing levels late last year, to the highest activity level since April 2022, which was when the rate hikes started.

But over the past two weeks, as mortgage rates spiked, the Refinance Mortgage Applications index re-plunged, according to the MBA today. Here is the detailed view:

On this longer-view chart, which includes the historic spike in refi applications during the 3%-mortgage era, we can see how refi applications (red) move inversely with mortgage rates (blue).

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the beer and iced-tea mug to find out how:

Would you like to be notified via email when WOLF STREET publishes a new article? Sign up here.

Source: wolfstreet.com